Cash “Is Still King” in Singapore

Ph.D. in U.S. History, Columbia University in the City of New York

Post-Doctoral Researcher in Global Correspondent Banking, 1870-2000 – Mexico and South America, University of Oxford

This post is also available in:

![]()

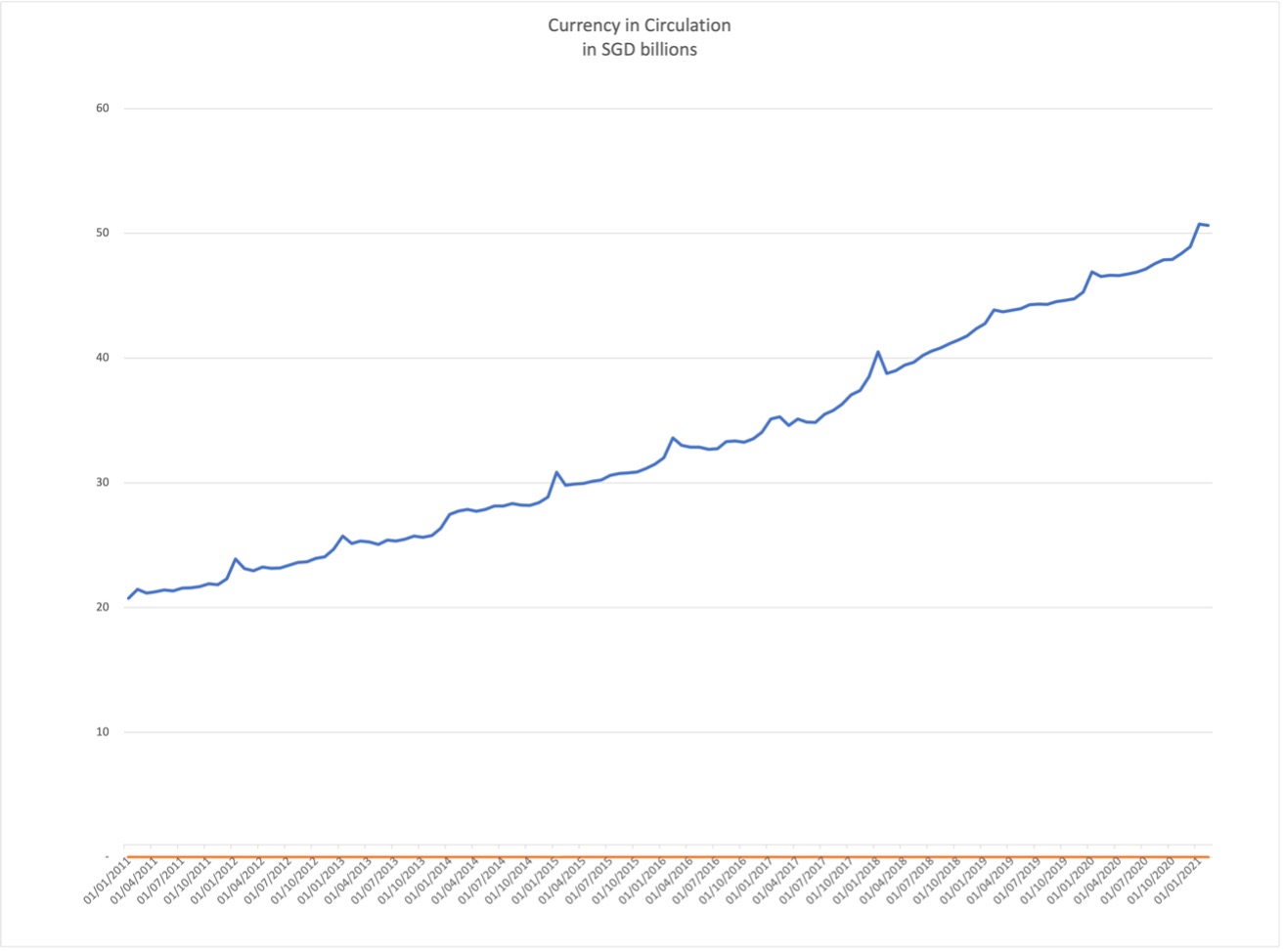

Currency in Circulation Expands, Despite a Fall in ATM Transactions

Monetary AuthoritySee Central Bank More of Singapore (MAS) data shows that in February 2021, currency in circulation reached 55.45 billion Singaporean dollars (S$, equivalent to US$41.35 billion), representing an annual increase of 9.5% (see Graph 1). ATM withdrawals decreased 16% during the Covid-19 pandemic, going from 205 million in 2019 to 172 million withdrawals in 2020. The withdrawals’ value decreased even more than the volume (20%), going from S$61.056 billion in 2019 (US$45.54 billion) to S$48.839 billion (US$36.42 billion) in 2020. The average value of ATM withdrawals registered a relatively small decline (5%), going from S$298 in 2019 (US$222) to S$283 in 2020 (US$211.06).

Graph 1. Singapore: CurrencyThe money used in a particular country at a particular time, like dollar, yen, euro, etc., consisting of banknotes and coins, that does not require endorsement as a medium of exchange. More in circulation, 2011-2021 (billions of Singaporean dollars)

Source: Monetary Authority of Singapore, CashMoney in physical form such as banknotes and coins. More Essentials.

The Business of Small Money Changers Collapses

Singapore has about 270 moneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More changers, most of them small, family-run firms. The collapse in business and leisure travel caused by border restrictions and lockdown measures to contain the spread of SARS-Covid-2 has negatively impacted Singaporean money changers. According to the MAS, 37 money changers have ceased business since April 2020, with five returning to operations, and 12 have closed permanently.

The Covid-19 pandemic has been the worst crisis for the sector, according to Mohamed Farook, 77, of Arcade Money Changers: “Even during the many financial crises and the SARS (severe acute respiratory syndrome) situation in 2003, we were not affected to this extent for such a prolonged period because our borders were still open and people were still travelling.” Another money changer reported that before the pandemic he used to sell up to 6 million Malaysian ringgits (RM, equivalent to US$1.45 million) a day: now he barely sells RM30,000 a day (US$7,258.65).

Hawkers Resist the Advent of Cashless Payments

Nearly half of all 18,000 Singaporean hawkers (itinerant and semi-permanent food merchants) started accepting cashless payments after authorities established a Hawkers Go Digital programme to incentivise digital solutions. The programme provided a S$300 bonus a month (US$225) if hawkers had at least 20 cashless payments monthly.

However, the programme has not brought a generalised adoption of cashless payments. A 58-year-old Airport Road hawker said, “Cash is still king among my customers… For us older hawkers, cash is more convenient – particularly during the rush hours, when juggling both cash and an e-payment system can be very troublesome.” A Toa Payoh hawker in his 60s with eyesight problems said, “It might waste even more time for me to try to handle the app, than just taking cash. Customers don’t want to be kept waiting either as I slowly key in the amount.”

Some customers have even found ways of cheating the hawkers out of their paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More, either by showing screenshots of earlier transactions or flashing pre-payment pages to later cancel transactions. Hawker Lum Sing Yew complained that he had lost S$150 with abusive customers: “It really hurts our earnings and these things add up… Going cashless is convenient, but if there are consistent monetary losses, maybe we should stick to cash.”

OCBC Bank Enables Face Verification in its ATM Network

OCBC Bank, the second-largest retail bank in Singapore, has recently announced it will allow users to employ face verificationChecking the authenticity. More to conduct transactions in its 550 ATMs. OCBC will scan customers’ faces in its ATMs and compare them to the images and identities of 4 million Singapore residents in the national biometric database (SingPass Face Verification) developed by the Government Technology Agency (GovTech).

Initially, OCBC will allow its clients to get their account balances in eight ATMs, followed by cash withdrawals. In 2022, face verification will extend to include cash deposits, fund transfers to other banks, cash card top-ups, and credit card bill payments. OCBC’s goal is to eliminate debit cards due to the risks of theft or cloning. Almost all OCBC ATMs are already contactless. The bank enabled QR cash withdrawals so that customers could leave their cards at home and scan a QR code to withdraw cash. In 2020, QR code cash withdrawals grew 88% year on year.

CashTech Solutions Accommodate Singaporeans’ Preference for Cash

Before the Covid-19 pandemic, Singapore was a country with very high levels of cash in circulationThe value (or number of units) of the banknotes and coins in circulation within an economy. Cash in circulation is included in the M1 monetary aggregate and comprises only the banknotes and coins in circulation outside the Monetary Financial Institutions (MFI), as stated in the consolidated balance sheet of the MFIs, which means that the cash issued and held by the MFIs has been subtracted (“cash reserves”). Cash in circulation does not include the balance of the central bank’s own banknotes (as... More given the size of its economy, according to the Asian Development Bank and the Bank of International Settlements. In 2019, Singapore had a currency in circulation to GDP ratio of 10.24%. In 2020, the ratio of currency in circulation to GDP grew to 12.2%.

OCBC and other entities are responding to Singaporeans’ preference for cash with digital innovations. Just in 2017, Singaporean cashtechThe expression was first coined by CashEssentials and is the encounter of cash and technology. It brings together innovative companies who leverage software and modern communications technology to improve cash services: access to cash; acceptance of cash; and the efficiency of the cash cycle for all stakeholders. More startup SoCash raised US$6 million in funding to expand its cash-in-shopService allowing a customer to withdraw cash from a payment account using a mobile application on a smartphone at a participating shop supporting the application. Also referred to as a “virtual ATM”. Unlike cashback, a cash-in-shop transaction does not require the consumer to make a purchase. More model in several Southeast Asian countries.

According to Sunny Quek, OCBC Singapore’s head of consumer financial services, “Singapore consumers are keen digital adopters – even the elderly. While cash is still a key mode of payment in Singapore, the digital overlay to get cash is very welcomed by consumers. Overall, digital adoption within OCBC has grown year-on-year in 2020 […]. With many customers already embracing QR cash withdrawals without having to use an ATM card, face verification will add a layer of convenience to more customers as they access our banking touchpoints.”

Singaporean customers are very comfortable using biometric authenticationThe process of proving that a banknote or security document is genuine. More methods, unlike people in other countries concerned about biometric data in big tech and government hands. Fingerprint and face recognition are emerging as “the new normal,” according to Kanv Pandit, group managing director for Asia Pacific banking solutions at processing and payments company FIS. “This is unsurprising as consumers cement their preferences for a quicker, more convenient and contactless experience when it comes to banking or paying, especially during the pandemic,” Pandit added.

This post is also available in:

![]()