Switzerland: The Resilient and Evolving Role of Cash

The survey, conducted among over 2,000 individuals, highlights that cashMoney in physical form such as banknotes and coins. More is not only widely accepted and used but also serves as a critical fallback and safeguard in an increasingly digital financial landscape.

The imprtance of cash is evidenced by its consistent use across diverse demographics, its role as a financial safeguard, and the high satisfaction levels among users regarding its acceptance and availability. The survey also underscores the public’s strong preference for maintaining cash as a paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More option, with only 2% advocating for its abolition. This sentiment reflects a collective recognition of the unique benefits of cash, including its immediacy, privacy, and universal accessibility—qualities that digital methods cannot fully replicate.

Moreover, the survey’s findings challenge the notion that cash is becoming obsolete. Instead, it suggests that cash and digital methods coexist, each serving distinct purposes. Cash remains particularly important for small transactions, inclusion, and as a backup in cases of technical disruptions or acceptance constraints. The positive evolution of cash in Switzerland is thus not just about its survival but about its adaptation and integration into a modern, multi-faceted payment ecosystem.

The Positive Evolution of Cash in Switzerland

The survey provides a comprehensive snapshot of cash’s role in Switzerland’s evolving payment landscape. Cash continues to play a significant and positive role in everyday transactions and financial resilience. This trend is further underscored by Switzerland’s recent decision to enshrine the right to cash in its constitution. In a landmark vote, the Swiss electorate overwhelmingly supported this measure, reflecting a deep societal commitment to preserving cash as a fundamental monetary option

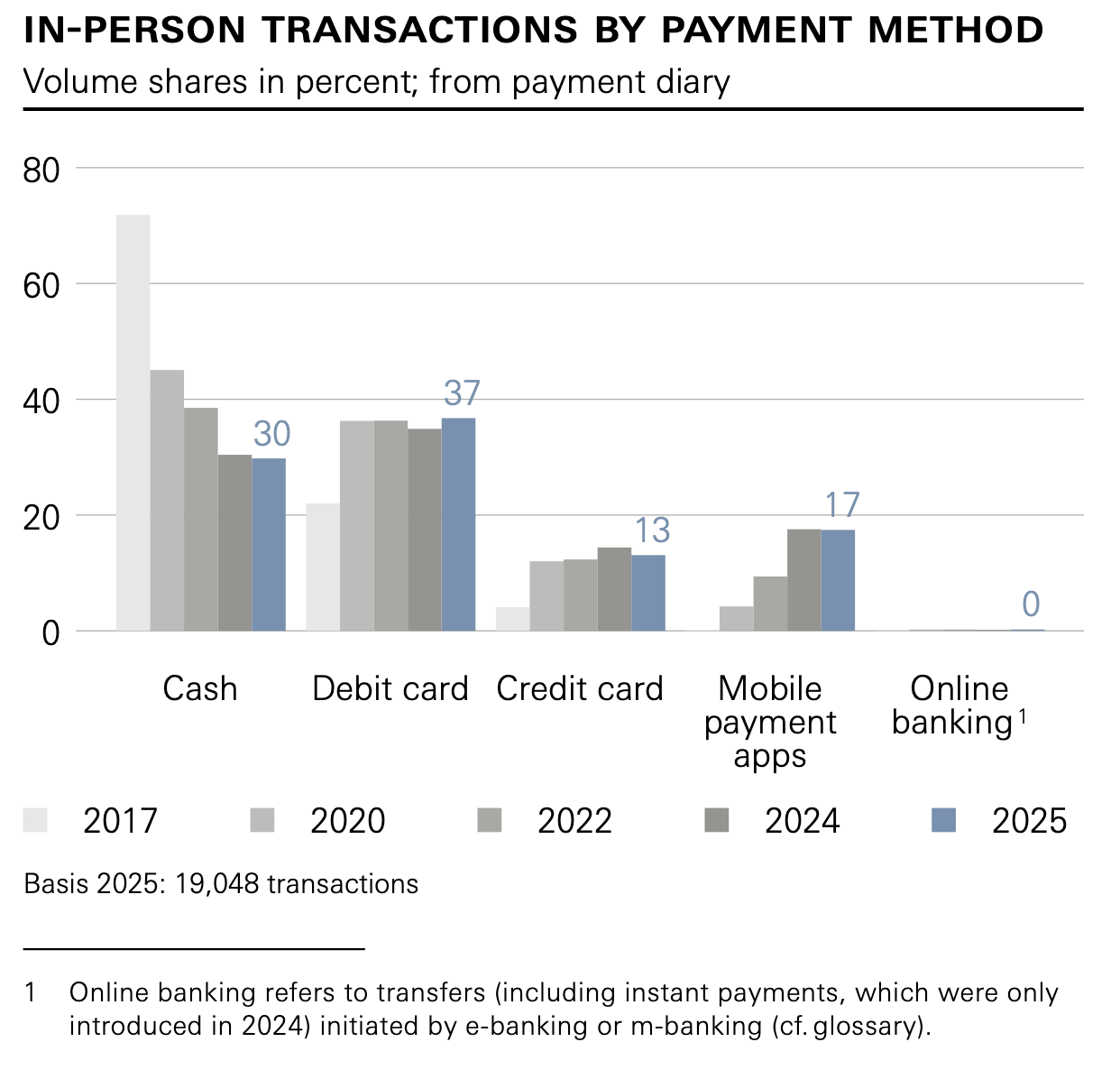

The survey confirms that cash is a regularly used payment methodSee Payment instrument. More in Switzerland, especially at physical points of sale (POSAbbreviation for “point of sale”. See Point-of-Sale terminal. More). While debit cards are the most frequently used method at POS, cash is the second most popular, followed by mobile payment apps. This consistent use of cash indicates its enduring relevance in everyday transactions. The chart below illustrates the evolution of in-person payment methods from 2017 to 2025, In 2025, debit cards were the most frequently used method (37%), followed by cash (30%), mobile payment apps (17%), and credit cards (13%). Online banking was not used for in-person transactions. Over the years, cash has steadily declined from 65% in 2017 to 30% in 2025, while debit cards, mobile payment apps, and credit cards have all increased in usage. This trend reflects a gradual shift toward non-cash payments, though cash remains a significant part of everyday transactions.

Source: SNB Payment Methods Survey of Private Individuals in Switzerland 2025

The role of cash is particularly pronounced in specific contexts: it is used more frequently for small transactions (under CHF 20), payments at small retailers, services outside the home, and when eating or drinking out. This aligns with the strengths of cash—speed, simplicity, and universal acceptance—making it a preferred choice for spontaneous, small-scale purchases.

The survey also notes that the volume share of cash has declined since 2020, but this decline is not uniform across all demographics. For example, people with lower incomes used cash more frequently in 2025 compared to 2024, suggesting that cash remains a critical tool for financial inclusionA process by which individuals and businesses can access appropriate, affordable, and timely financial products and services. These include banking, loan, equity, and insurance products. While it is recognised that not all individuals need or want financial services, the goal of financial inclusion is to remove all barriers, both supply side and demand side. Supply side barriers stem from financial institutions themselves. They often indicate poor financial infrastructure, and include lack of ne... More and accessibility.

High Satisfaction and Acceptance of Cash

Satisfaction with cash acceptance remains exceptionally high among Swiss residents. Nearly all respondents (98%) state they are satisfied or mostly satisfied with cash acceptance, underscoring its widespread and reliable availability.

Cash also plays a crucial role as an alternative payment method when other methods fail. In about half of the cases where acceptance constraints or technical disruptions occur, cash is used to complete the transaction. This adaptability highlights its importance as a fallback in an increasingly digital payment ecosystem.

The survey reveals that cash is not just a payment method but a symbol of financial autonomy and choice. The fact that only 2% of respondents favour abolishing cash reflects a strong societal preference for maintaining this option, even as digital methods advance.

Cash as a Financial Safeguard and Tool for Inclusion

A significant proportion of Swiss residents (69%) keep cash at home or in a safety deposit box, with 63% doing so for everyday expenses and 33% as a reserve for unforeseen circumstances, technical disruptions, or crises. This trend has increased over the past five years, reflecting a growing recognition of the role of cash in financial preparedness.

The utility of cash as a financial safeguard is further emphasized by the fact that 89% of respondents carry cash in their wallets. This widespread habit ensures that cash is always accessible, providing peace of mind and financial flexibility in both routine and unexpected situations.

The survey also highlights its importance for socio-economic inclusion. For individuals who may not have access to digital banking or prefer not to use it, cash remains the most accessible and inclusive payment method. Its universal acceptance and lack of reliance on technology or intermediares make it a vital tool for ensuring no one is left behind in the digital transition.

Cash in the Context of a Digital Economy

The coexistence of cash and digital payment methods reflects a balanced and pragmatic approach to financial transactions. While digital methods offer convenience and speed, cash provides immediacy, privacy, and reliability—qualities that are irreplaceable in certain contexts.

The survey’s findings challenge the narrative of the decline in cash, instead showcasing its adaptive role. Cash is not disappearing but evolving, serving as a complementary rather than competing payment method. Its use in small transactions, as a backup, and for financial inclusion demonstrates its continued relevance in a modern economy.

The Swiss public’s strong preference for maintaining cash as a payment option (only 2% advocate for its abolition) signals a collective understanding of its unique benefits. Cash’s role in economic resilience, especially during crises or technical disruptions, further solidifies its importance in the payment ecosystem.

Conclusion

The 2025 SNB survey paints a clear picture: cash is not on the verge of obsolescence but is evolving to meet the needs of a modern, digital economy. Its resilience, adaptability, and role as a financial safeguard make it an indispensable part of Switzerland’s payment landscape. As digital methods continue to advance, cash’s positive evolution highlights the value of maintaining a diverse and inclusive payment ecosystem—one where cash and digital coexist to serve the needs of all Swiss residents.