A Tale of Transactions: An Analysis of Retail Payments in the Euro Area

Diederik Bruggink has recently published an analysis of retail payments of the euroThe name of the European single currency adopted by the European Council at the meeting held in Madrid on 15-16 December 1995. See ECU. More area in the peer-reviewed Journal of Payments Strategy and Systems.

Cash is used for low-value transactions and as a precautionary reserve

The paperSee Banknote paper. More offers a detailed, data-driven exploration of how Europeans actually pay in their daily lives. Drawing on the European Central Bank’s SPACE 2024 study and transaction data, it examines the realities of retail paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More behaviour. This perspective is particularly important in the context of ongoing discussions about a potential holding limit for the digital euro. Whilst the paper examines cashMoney in physical form such as banknotes and coins. More, cards and e-money transactions, all presented in Table 1, this summary for Cash Essentials notably addresses the cash-related aspects.

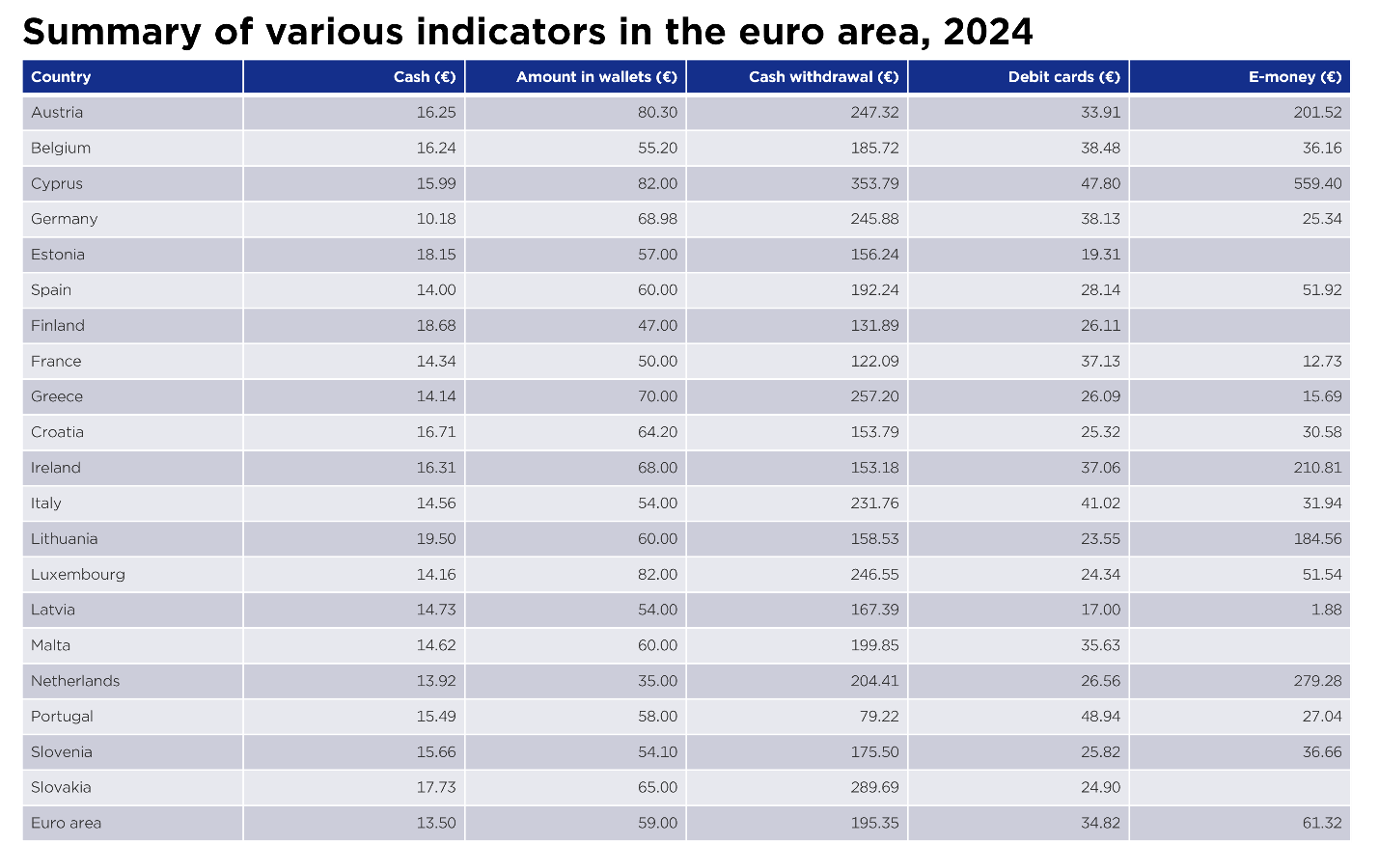

Table 1: Summary of various indicators in the euro area, 2024

At the heart of the analysis lies a careful examination of cash. Contrary to common narratives about its decline, the paper shows that cash continues to play a meaningful and nuanced role in the euro area. Three key indicators – also presented in Table 1 and summarised visually in Figure 1 – capture this role: the average value of a cash transaction (€13.50), the amount of cash people carry in their wallets (€59), and the average size of ATM withdrawals (around €195). Taken together, these figures reveal a striking duality. Cash is still primarily used for small, everyday transactions, yet it is also held in relatively large amounts as a precautionary reserve.

The evolving role of cash

This dual function is one of the most important insights of the paper. The low average transaction value confirms that cash remains deeply embedded in routine spending, such as groceries, cafés, or small services. At the same time, the fact that consumers carry nearly €60 on average – and withdraw almost €200 at a time – suggests that cash is valued not only as a payment instrumentDevice, tool, procedure or system used to make a transaction or settle a debt. More but also as a form of readily available liquidityDescribes the extent to which assets or rights can be converted into cash without causing a significant decrease in the asset’s price. Accordingly, liquidity is often inversely proportional to the profitability of the asset and involves the trade-off between the selling price and the time needed to convert it to cash. In finance, cash is considered the most liquid asset and cash is sometimes used as a synonym for liquidity (e.g. cash reserves; cash pooling…). More. In other words, cash is not disappearing; rather, its role is evolving. It is being used less frequently, but when it is used or held, it continues to serve an important function as a fallback or safety buffer.

The data also highlight significant differences across countries, reinforcing the idea that payment behaviour remains culturally and structurally diverse within the euro area. In countries such as Germany and Austria, cash is still central to everyday transactions. Consumers in these countries tend to carry relatively large amounts of cash and use it frequently for small purchases, which is reflected in low average transaction values combined with high wallet holdings. By contrast, in more digitally advanced economies such as the Netherlands and Finland, cash plays a much more limited role. People carry less cash and tend to use it only occasionally, often for somewhat larger payments. Between these two extremes lies a broad middle group – including countries such as Belgium, Spain, and Italy – where cash continues to coexist with cards and digital payments in a more balanced way.

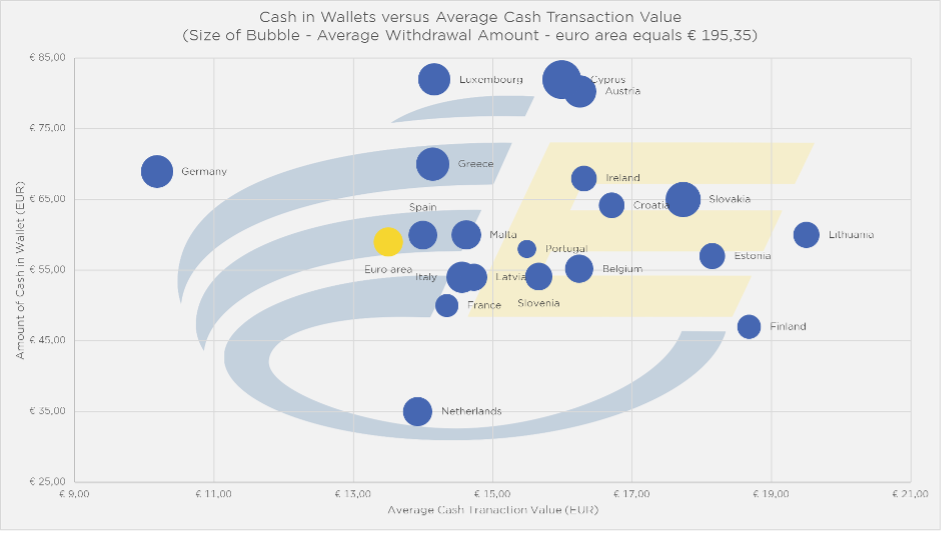

Figure 1: Overview of three cash-related indicators per country in the euro area

Figure 1 brings these patterns together by showing how the three indicators – transaction value, wallet holdings, and withdrawals – interact across countries. What emerges is a consistent picture of cash transitioning toward a “low-frequency but high-relevance” instrument. Even in countries where digital payments dominate, cash is not abandoned; instead, it is retained for specific situations, emergencies, or as a general-purpose backup. The upward trend in average withdrawal amounts reinforces this interpretation, suggesting that people are visiting ATMs less often but withdrawing larger sums when they do.

An additional and somewhat surprising finding concerns the relationship between cash and the shadow economy. While cash is often associated with informal or undeclared economic activity, the analysis finds no strong correlation between the two. The link between average cash transaction values and the size of the shadow economy is weak, and there is no meaningful relationship for wallet holdings or withdrawal behaviour. This suggests that most observed cash usage reflects legitimate consumer behaviour rather than hidden economic activity, challenging a common assumption in policy discussions.

When cash is placed in the broader context of other payment methods, its evolving role becomes even clearer. Debit cards have become the dominant instrument for retail payments in the euro area, with an average transaction value of €34.82 and a clear trend toward use in smaller, everyday purchases. This reflects the growing importance of contactless payments and digital wallets, which have made card payments increasingly convenient for low-value transactions. E-money, by contrast, remains relatively marginal and unevenly distributed, with most transactions concentrated in just a few countries. As a result, cards – not e-money – are the primary substitute for cash in daily life.

Cash is an essential and trusted component of financial behaviour

These findings have important implications for the potential introduction of a digital euro. The analysis underscores how slowly payment habits tend to changeThis is the action by which certain banknotes and/or coins are exchanged for the same amount in banknotes/coins of a different face value, or unit value. See Exchange. More. Historical examples, such as the gradual decline of cheques in favour of cards, show that substitution between payment methods can take many years, even decades. While the shift from cash to digital payments has accelerated in recent years, it is still shaped by deeply ingrained habits, infrastructure, and trust. This means that a digital euro is more likely to complement existing payment methods than to replace them outright.

In conclusion, the paper paints a nuanced picture of the euro area payment landscape. Cash is no longer dominant in terms of transaction volume, but it remains an essential and trusted component of everyday financial behaviour. Its continued use reflects not only its role in small transactions but also its importance as a store of liquidity. For policymakers, this implies that the success of a digital euro will depend less on its technical design alone and more on how well it aligns with these established patterns of behaviour.