The Price of Paying: New insights on Retail Payment Costs in Germany

Why Payment Costs Matter

The way consumers pay in shops has been changed significantly in recent years. Alongside cashMoney in physical form such as banknotes and coins. More and traditional cards, digital paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More methods such as smartphone and smartwatch payments are becoming increasingly common. For retailers, however, every payment methodSee Payment instrument. More comes with costs – even if consumers themselves usually do not directly pay for making a transaction.

A new study by the Deutsche Bundesbank examines these costs in detail and provides one of the most comprehensive analyses of payment costs in the German retail sector to dateThe year in which a medal or coin was minted. On a banknote, the date is usually the year in which the issuance of that banknote - not its printing or entering into circulation - was formally authorised. More. The study analyses both monetary costs – such as transaction fees, terminal costs or cash handling expenses – and non-monetary costs, especially the time required to process payments. It combines around 13,000 transaction time measurements with survey data from 268 firms across retail.

Cash and Girocard are the Most Cost-effective Options

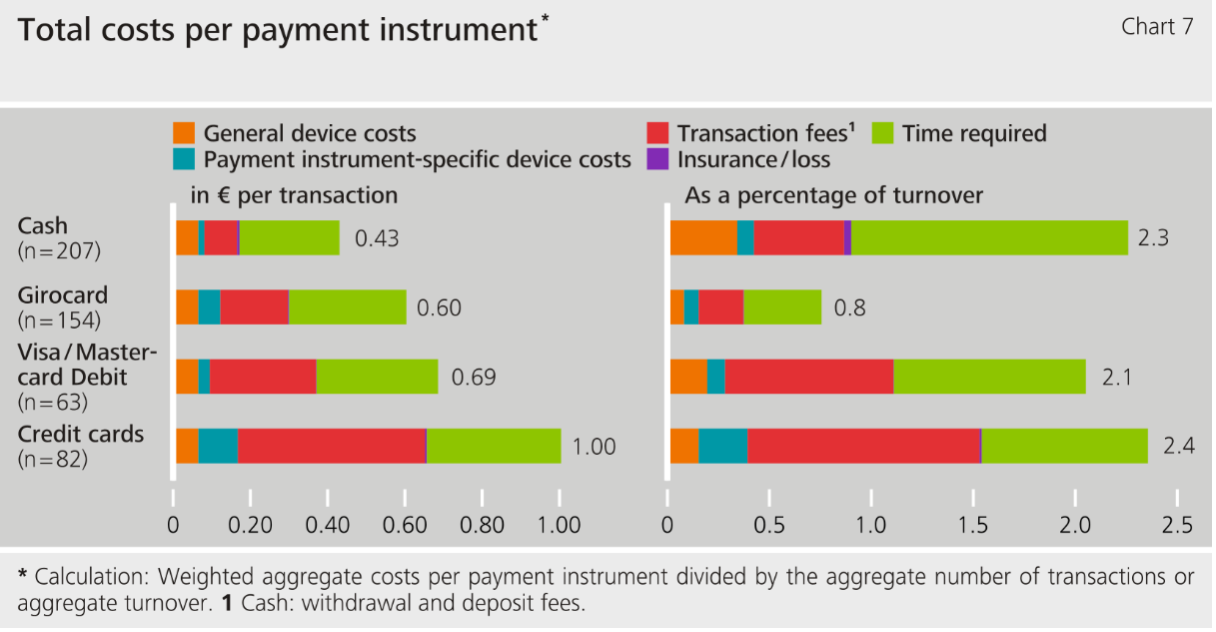

One of the central findings is that cash and girocard [Girocard is Germany’s domestic debit card scheme] remain the most cost-effective payment methods for merchants in Germany. However, the result depends on the perspective used. When analysing costs per transaction, cash performs best, with average costs of €0.43 per payment. Girocard transactions costs around €0.60 on average. The picture changes when costs are measured relative to turnover. In this case, girocard becomes the most efficient option, with costs amounting to around 0.8% of turnover, while cash reaches roughly 2.3%. International debit cards such as Visa Debit and Mastercard Debit, as well as credit cards, are significantly more expensive for merchants overall. Credit cards, for example, generate average costs of €1.00 per transaction and around 2.4% of turnover.

The study also highlights that the structure of costs differs substantially between payment methods. For cash payments, time costs play a particularly important role. Staff must count banknotes and coins, provide changeThis is the action by which certain banknotes and/or coins are exchanged for the same amount in banknotes/coins of a different face value, or unit value. See Exchange. More, prepare deposits and reconcile cash balances. By contrast, card-based payments are heavily influenced by transaction fees charged by payment service providers and card schemes.

International Cards Generate Higher Merchant Costs

There are significant differences in transaction fees between card systems. Girocard has the lowest average fees among the analysed card-based payment methods, whereas international debit cards and especially credit cards are associated with substantially higher charges. The findings suggest that scheme fees and other payment processing costs play an increasingly important role for retailers when international card networks are used. This is particularly relevant in an environment where cashless payments continue to gain market share and where international card schemes are becoming more widespread.

International comparisons demonstrate that payment costs vary strongly across countries. Factors such as payment habits, market structures, transaction sizes and regulatory frameworks all influence the cost structure of payment methods. Still, the German results fit into a broader international pattern in which national debit card schemes often prove relatively cost-efficient, while international card systems tend to generate higher merchant costs.

Smaller Businesses Face Higher Relative Costs

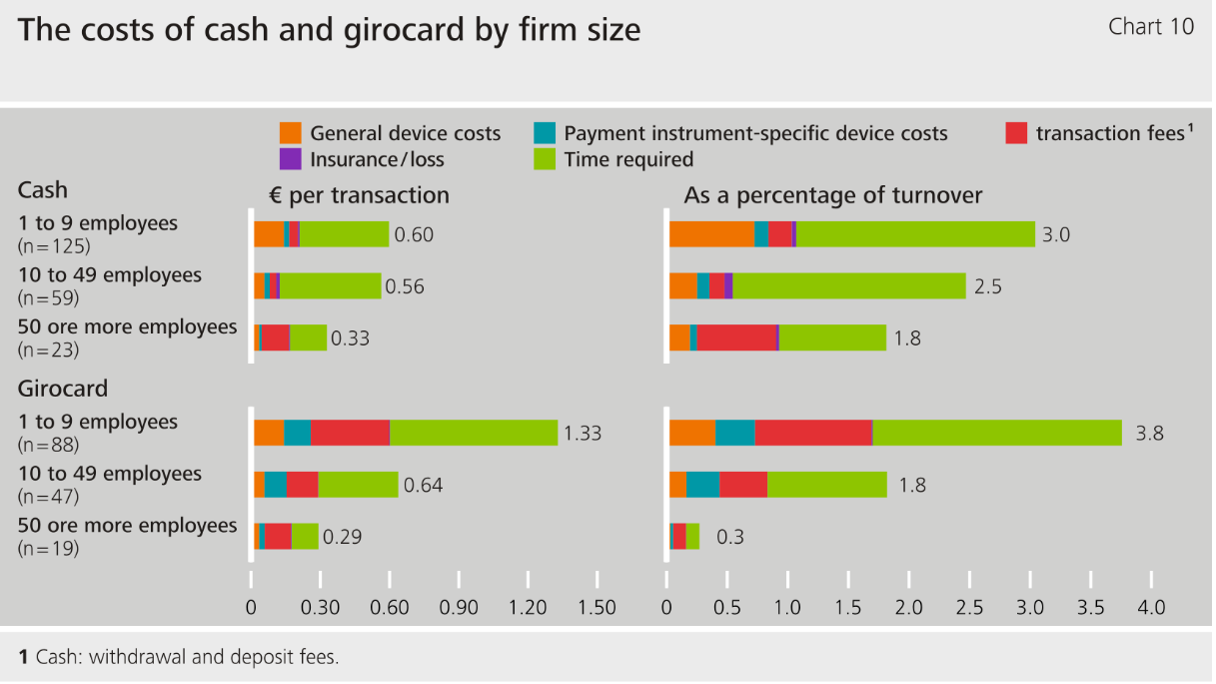

Another important finding concerns the role of firm size. Larger companies generally face significantly lower payment costs than smaller businesses. Economies of scale allow larger firms to spread fixed costs over more transactions and negotiate better conditions with payment providers. This effect is especially visible for cashless payment methods. Small firms often face relatively high transaction fees and equipment costs, which can become a barrier to accepting additional payment methods.

The acceptance rates of payment methods also differ considerably across firm sizes. Cash remains almost universally accepted, with an acceptance rate of 98% among surveyed firms. Girocard follows with 73%, while international debit cards and credit cards are accepted by roughly half or merchants. Acceptance of cashless methods is especially high among larger retailers, whereas smaller business are more cautious, partly due to the associated costs.

Mobile Payments are Becoming Mainstream

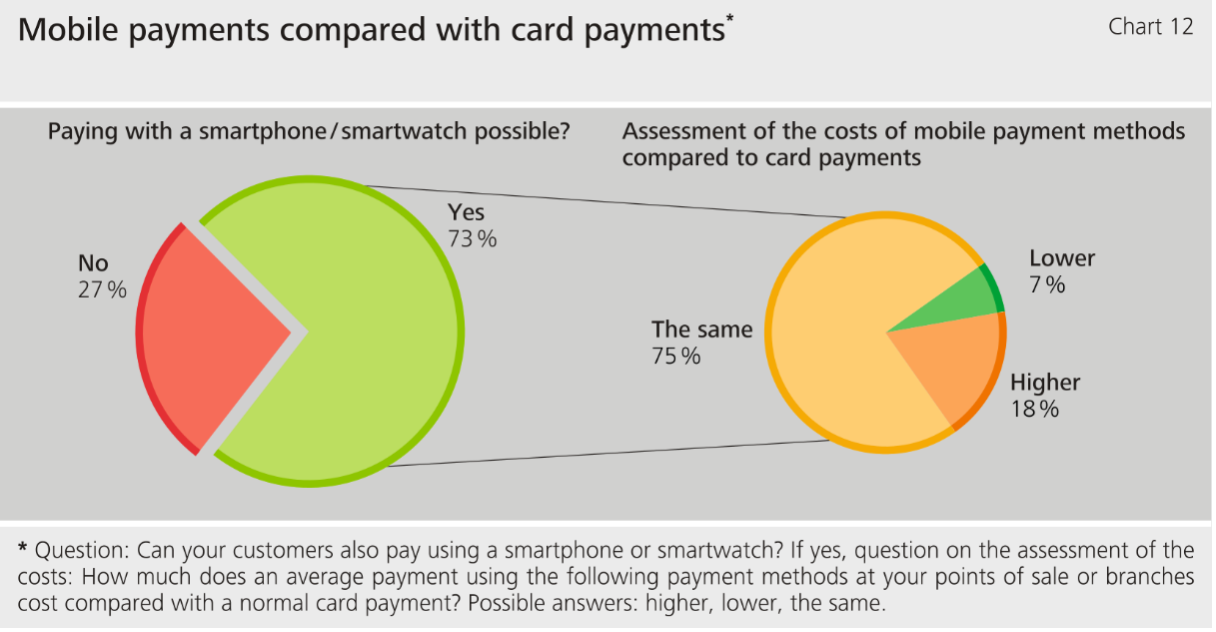

The study further shows that mobile payments have become an established part of the payment landscape in Germany. Around 73% of card-accepting firms already allow payments via smartphone or smartwatch. Most merchants perceive the costs of mobile payments to be broadly comparable to traditional card payments, since mobile wallets are typically linked to existing debit or credit card infrastructures. This suggests that, from a merchant perspective, mobile payments are currently often perceived less as a separate payment method and more as an extension of existing card payment systems. At the same time, the findings underline the growing importance of digital and mobile payment solutions in everyday retail payments.

Why the Results Matter for the Future of Payments

From a policy perspective, the findings are highly relevant. Payment systems are a central part of economic infrastructure, and understanding their costs is essential for ensuring efficiency, competition and consumer choice. The Bundesbank emphasises that both cash and cashless payment methods should be widely available and cost-efficient to ensure that customers have the freedom to choose their preferred method of payment. The study also underlines the importance of transparency: only when payment costs are clearly understood can policymakers, central banks and market participants make informed decisions about the future of payments.

The results are particularly timely given ongoing discussions about digital payments and the potential introduction of a digital euroThe name of the European single currency adopted by the European Council at the meeting held in Madrid on 15-16 December 1995. See ECU. More. Retailers increasingly accept innovative payment solutions, while at the same time many businesses still value the role of cash and the existing cash infrastructure. The study therefore contributes not only to the academic debate on payment costs, but also to wider discussions about competition, efficiency and resilience in modern payment systems.

Fabio Knümann is a Senior Economist in the cash department at the Deutsche Bundesbank. He is responsible for topics such as cost of payment and cash infrastructure. The article represents the author’s personal opinions and does not necessarily reflect the views of the Deutsche Bundesbank or the EurosystemThe Eurosystem comprises the European Central Bank and the national central banks of those countries that have adopted the euro. More. It is based on the study “The costs of payment methods in the retail sector”, authored by Niklas Ego (Deutsche Bundesbank), Fabio Knümann (Deutsche Bundesbank) and Lukas Korella (Deutsche Bundesbank).