After Sweden, the UK will Protect the Future of Cash by Legislation

This post is also available in:

![]()

Cash in CirculationThe value (or number of units) of the banknotes and coins in circulation within an economy. Cash in circulation is included in the M1 monetary aggregate and comprises only the banknotes and coins in circulation outside the Monetary Financial Institutions (MFI), as stated in the consolidated balance sheet of the MFIs, which means that the cash issued and held by the MFIs has been subtracted (“cash reserves”). Cash in circulation does not include the balance of the central bank’s own banknot... More is growing again in Sweden

According to data from the Riksbank, the value of cashMoney in physical form such as banknotes and coins. More in circulation was almost halved between 2007 and 2018. The decline was continued but quite irregular: it was below 5% per year between 2007 and 2012 but then accelerated to two-digit rates in 2013, 2015 and 2016. At that point, many observers projected that cash would disappear altogether in Sweden before the end of the following decade. But then, rather unexpectedly, in May 2018 the curves crossed. Cash in circulation grew by 7.2% in 2018 and 2.1% in 2019.

Sweden passes legislation

A new law came into effect on January 1st requiring banks to provide an adequate level of cash services. The law was designed to protect the more fragile people such as the elderly, migrants, those with disabilities, the rural or those who do not have access to digital payments.

The law, officially named the Obligation for Certain Credit Institutions to Provide Cash Services, was announced by finance minister Per Bolund in June 2019, submitted to parliament in September, and voted by the end of November. Bolund emphasised that the government wanted to make sure that it would continue to be possible to take out and pay in cash, even in rural Sweden.

Big banks will have a special responsibility to maintain cash services across the whole country

“Unfortunately, banks have continued to reduce their cash services, especially in sparsely populated areas. This proposal means that the big banks will have a special responsibility to maintain cash services across the whole country,” Bolund said.

The Swedish Post and Telecom Authority, which oversees the implementation of the new law, will ensure that banks holding over 70 billion SEK in deposits will offer cash services across the country. The banking regulator, the Financial Supervisory Authority, may issue financial penalties if banks fail to comply. 2020 will be a pilot phase, as the law enters into force on January 1, 2021.

This is only a partial victory if it isn’t now followed up by the retail industry taking cash

Björn Eriksson, head of the pro-cash lobby Kontantupproret (Cash Protest), said the fight for those who wanted to keep using cash was not over. “This is only a partial victory if it isn’t now followed up by the retail industry taking cash. That will be the next big battle.”

The Swedish Civil Contingencies Agency which advised consumers to stash cash in case of a war or cyberattack in 2018, suggested that supermarkets, pharmacies, petrol stations, and health services (those that are most important during an emergency) must be required to accept cash.

The new law requires banks to ensure that everyone can withdraw cash. It does not set a limit to the maximum number of kilometers citizens should have to travel to access an ATM. Banks will also needs to offer cash deposit services to businesses but not to consumers. The responsibilities may be delegated to a cash managementManagement and control of cash in circulation. More company or a retailer.

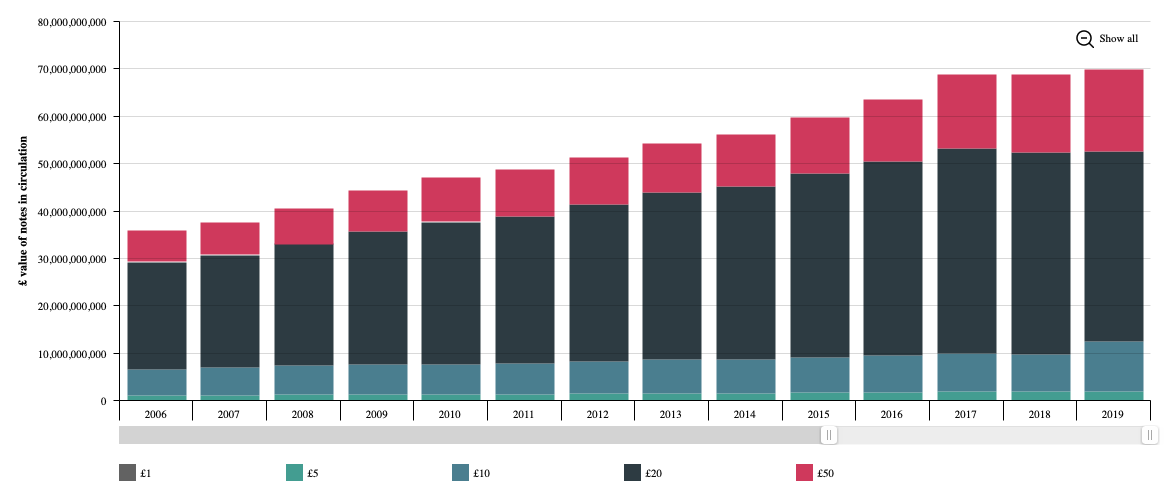

Growth of Cash in Circulation has been flattening in the UK

Cash in circulation has followed a very different evolution in the UK than in Sweden. It has doubled between 2005 and 2017 and grew at an annual rate of 8.3% in 2017. But growth has flattened since with 0% in 2018 and 1.4% in 2019.

Value of Notes in Circulation

Source Bank of England.

The UK is following Sweden’s footsteps

In the UK, the Treasury has also committed to the future of cash and promised to introduce legislation to protect access for those who need it. The Treasury will begin talks with industry and regulators – including the Bank of England, the Financial Conduct Authority (FCA) and PaymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More Systems Regulator – immediately after the Budget, to ensure that the industry “continues to meet the changing needs of cash users” and safeguards the sustainability of the UK’s cash infrastructure.

A quarter of ATMs charge customers to withdraw their moneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More

Last month, the independent Access to Cash review warned that cash use had reached a “tipping point”, as the rate of decline accelerated faster than expected and that cash would collapse in the absence of legislation. It is estimated that around 2.2 million people in the UK are still reliant on cash, with the elderly, vulnerable and those in rural communities likely to be hardest hit by a decline. One quarter (25%) of all ATMs now charge customers to withdraw their own money (up from 7% a year ago); the collapse of the cash withdrawal service at the Post Office was only narrowly averted in November 2019 in the face of public pressure; and increasing numbers of small and large business are ‘going cashless’ in the face of the rising costs of banking cash leaving some consumers unable to access services.

“The announcement today put us on the right track to maintain a viable cash system in the UK while so many people need it, without the risk of millions of people being left behind,” said Natalie Ceeney, independent chair of the Access to Cash Review.

A single regulator in charge of protecting cash

Anabel Hoult, CEO of consumer group Which?, said: “We know that the cash system faces irreversible damage within the next two years, so the government must swiftly press ahead with its plans to legislate, which must include putting a single regulator in charge of protecting cash.”

The Treasury announces it would look at how other countries have intervened to save cash, including Sweden. It will also look at giving the bank new powers to ensure they properly support customers’ cash needs and a new system for banks to move money around the country.

Will it be enough?

In both countries, the approach is aimed at delaying the ‘tipping point’ rather than triggering a cash revival. The approach requires that banks play along and beyond the simple compliance with the new regulations and provide convenient and cost-efficient access to cash. It remains to be seen if a strictly regulatory approach will be enough.

This post is also available in:

![]()