ECB welcomes Swedish draft law ordering banks to provide cash services

This post is also available in:

![]()

On 26 November, the ECB has published a non-legally binding opinion on the legislative proposal put forward by the Swedish government on 26 September 2019 requiring that large credit institutions provide cashMoney in physical form such as banknotes and coins. More services to the public. The purpose of the law is to ensure an adequate level of access to cash throughout Sweden in a context of ATM closures and branches which no longer enable cash deposits or withdrawals.

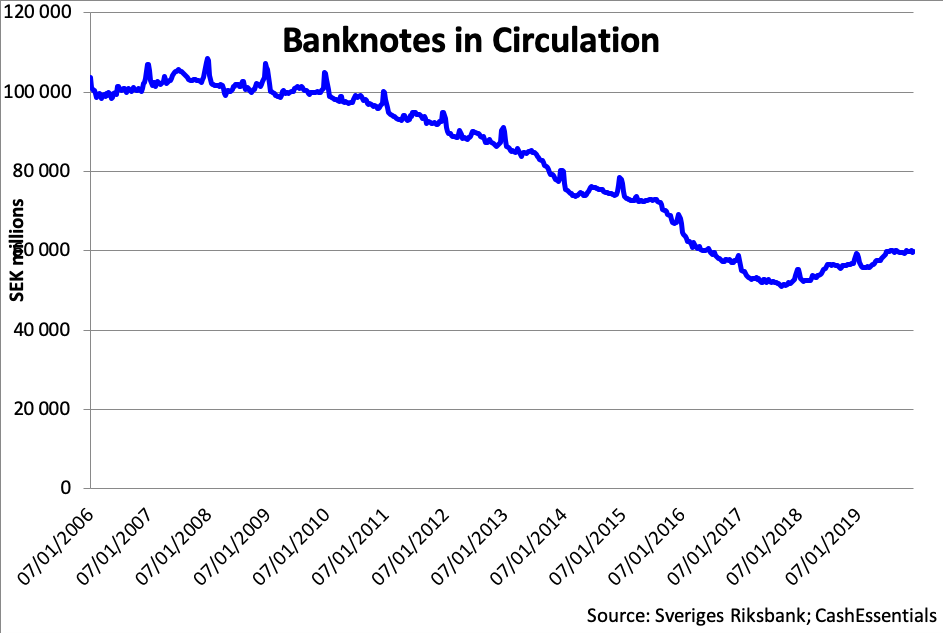

The value of cash in circulationThe value (or number of units) of the banknotes and coins in circulation within an economy. Cash in circulation is included in the M1 monetary aggregate and comprises only the banknotes and coins in circulation outside the Monetary Financial Institutions (MFI), as stated in the consolidated balance sheet of the MFIs, which means that the cash issued and held by the MFIs has been subtracted (“cash reserves”). Cash in circulation does not include the balance of the central bank’s own banknot... More has been halved between 2007 and 2018, dropping from SEK 111 billion to SEK 57 billion. But it has been increasing again since early 2018 as illustrated in the chart below.

The draft law applies to 6 financial institutions which hold deposits exceeding SEK 70 billion. The banks would be required to provide withdrawal services to consumers as well as deposit services for businesses.

“The ECB considers it important that all Member States, including non-euro area Member States, take appropriate measures to ensure that credit institutions and branches operating within their territories provide adequate access to cash services, in order to facilitate the continued use of cash.”

The proposal underlines that cash remains crucial for certain groups, including the elderly, immigrants, the disabled, socially vulnerable citizens and others with limited access to digital services. This could lead to disruptions in case of a contingency or malfunction of the paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More system. The ECB notes that “the ability to pay in cash remains particularly important for certain groups in society that, for various legitimate reasons, prefer to use cash rather than other means of payment, or who are unable to use digital technology. Additionally, cash payments facilitate the inclusion of the entire population in the economy by allowing it to settle any kind of financial transaction in this way”.

In October 2018 the Riksbank had also welcome the initiative as a step in the right direction. The Riksbank had suggested however that the obligation should be extended to all banks. It also called for the clarification of the legal tenderMoney that is legally valid for the payment of debts and must be accepted for that purpose when offered. Each jurisdiction determines what is legal tender, but essentially it is anything which when offered (“tendered”) in payment of a debt extinguishes the debt. There is no obligation on the creditor to accept the tendered payment, but the act of tendering the payment in legal tender discharges the debt. More status, stipulating that “activities that are important from a citizen’s perspective shall be obliged to accept cash (for example pharmacies, special transport services, food shops, petrol stations).”

This post is also available in:

![]()