The Rebound of Cash in Australia Amid Declining Infrastructure

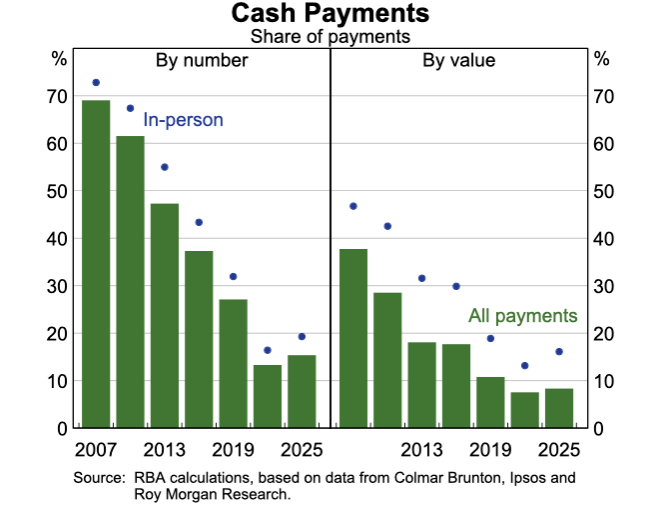

After decades of steady decline, cashMoney in physical form such as banknotes and coins. More is making a surprising comeback in Australia. According to the Reserve BankSee Central bank. More of Australia’s (RBA) 2025 Consumer Payments Survey, cash now accounts for 15% of all payments, with 50% of Australians using cash in a typical week. This rebound reveals a more complex and nuanced relationship between consumers and cash. However, this resurgence coincides with a troubling trend: the decline of cash infrastructure, particularly for deposit services, which threatens to undermine access to cash for those who rely on it most.

The Rebound of Cash: A Shift in Consumer Behaviour

The RBA’s 2025 survey highlights a notable reversal in the decline of cash usage. After years of decreasing cash payments, both in volume and in value, Australians are once again turning to it for a significant portion of their transactions. This shift is particularly evident among certain demographics, including older Australians, low-income households, and those in regional and remote areas.

Factors Behind the Rebound include:

Factors Behind the Rebound include:

- Trust and Resilience: Cash is perceived as a trustworthy fallback in an era of increasing cyber threats and digital paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More outages. High-profile incidents, such as the 2023 Optus data breach and periodic failures of digital payment systems, have reminded consumers of the risks associated with relying solely on electronic transactions.

- Privacy Concerns: As awareness of data tracking and surveillance grows, many Australians are turning to cash to preserve their privacy. Unlike digital payments, which leave a traceable trail, cash transactions are anonymous.

- Budgeting and Control: Cash provides a tangible way to manage spending. Studies show that people tend to spend less when using physical currencyThe money used in a particular country at a particular time, like dollar, yen, euro, etc., consisting of banknotes and coins, that does not require endorsement as a medium of exchange. More, as the act of handing over cash creates a psychological “pain of paying” that digital transactions lack.

- Cultural and Social Factors: Cash remains deeply embedded in certain social and cultural practices, such as small businesses, markets, and community events.

Cash continues to play a vital role in Australia’s payment landscape. The RBA’s survey reveals that half of all Australians use cash in a typical week, demonstrating its enduring relevance.

The Decline of Cash Infrastructure: A Looming Crisis

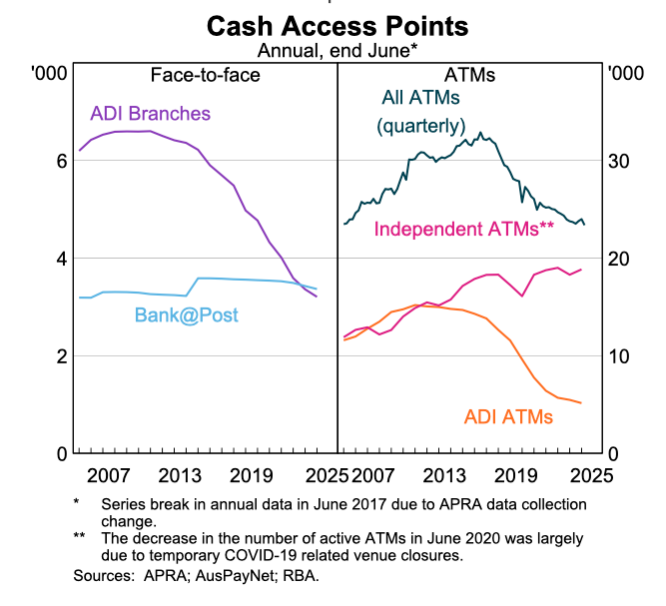

Despite cash’s resurgence in usage, the infrastructure that supports it is rapidly deteriorating. The RBA’s survey highlights a concerning trend: access to cash deposit services is declining, particularly in regional and remote areas.

The decline in the cash infrastructure is driven by a fall in bank branches and bank-owned ATMs. The growth of independent ATM numbers odes not compensate the decline of bank-owned devices. Furthermore, cash access points offered by banks generally provide a broader range of cash services and particulary deposit and are less likely to charge fees. Small businesses may also find it more difficult to get cash for their tills and deposit their earnings if they do not have convenient access to banking services. In early 2025, the four major banks committed to a moratorium on branch closures in regional areas until at least mid-2027, to help maintain banking services for regional communities.

The deterioration of cash infrastructure has serious implications for financial inclusionA process by which individuals and businesses can access appropriate, affordable, and timely financial products and services. These include banking, loan, equity, and insurance products. While it is recognised that not all individuals need or want financial services, the goal of financial inclusion is to remove all barriers, both supply side and demand side. Supply side barriers stem from financial institutions themselves. They often indicate poor financial infrastructure, and include lack of ne... More, economic resilience, and social equity.

Key Consequences include:

- Exclusion of Vulnerable Groups: The decline in cash deposit services disproportionately affects older Australians, low-income individuals, and those in regional areas.

- Increased Financial Vulnerability: As cash becomes harder to access, those who rely on it may be forced to adopt digital payment methods that they are uncomfortable with or unable to use effectively.

- Erosion of Trust in the Financial System: If cash infrastructure continues to decline without adequate alternatives, it could undermine trust in the financial system.

- Economic Inefficiency: Cash plays a critical role in informal economies, small businesses, and community transactions.

Policy Responses: Preserving Cash Access

Recognizing the importance of cash and the challenges posed by declining infrastructure, policymakers and financial institutions in Australia are beginning to take action.

Potential Solutions include :

- Mandating Cash Deposit Services: Governments could require banks to maintain a minimum level of cash deposit services.

- Public-Private Partnerships: Collaboration between governments, banks, and fintech companies could help fund and maintain cash infrastructure.

- Support for Cash-Based Businesses: Policymakers could provide tax incentives or grants to small businesses that accept cash.

- Consumer Education and Awareness: Public campaigns could raise awareness about the importance of cash and the need to advocate for its preservation.

- Innovation in Cash Infrastructure: New technologies, such as smart ATMs or mobile cash deposit services, could help modernize cash infrastructure.

The Future of Cash in Australia: A Call to Action

The rebound of cash in Australia is a reminder that cash remains a vital part of the payment landscape. However, its future is uncertain without urgent action to address the decline of cash infrastructure. It is critical that policymakers, financial institutions, and consumers work together to preserve access to cash for those who need it most.