The ECB’s Debate on CBDCs is Mainly Analytical

This post is also available in:

![]()

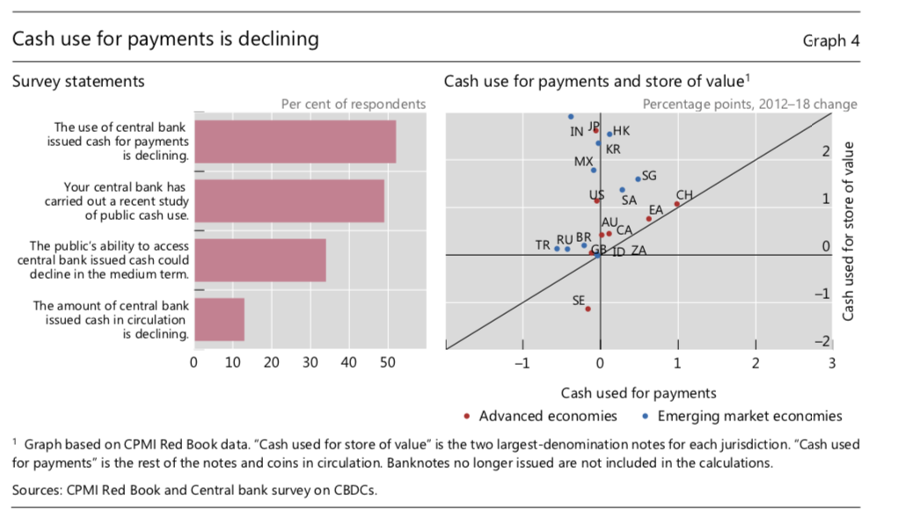

According to a survey published in January by the Bank for International Settlements (BIS), 80% of central banks are engaging in some kind of work in relation to CBDC. However, only 40% have evolved from research to experiments or proofs-of-concept and less than 10% are running pilots, all of which come from emerging markets. These numbers have actually declined between 2018 and 2019, as illustrated by the charts below.

The BIS survey also highlights that the evolution of cashMoney in physical form such as banknotes and coins. More demand is a major motivation leading central banks to investigate CBDCs. For some, CBDCs could reduce the high reliance on cash whereas for others, declining transactional demand for cash could be offset by a CBDC which would provide access to central bank moneyA liability of a central bank, including banknotes in circulation and banks’ deposits with the central bank. More for the general public. Just under half of the world’s central banks are investigating the public’s use of cash and a third are concerned that access to cash could decline in the medium term.

There is no trend away from cash in the euroThe name of the European single currency adopted by the European Council at the meeting held in Madrid on 15-16 December 1995. See ECU. More area

This is not the case however at the ECB. Speaking at a virtual conference about the future of moneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More, Yves Mersch has stated in a speech “While electronic payments are already crowding out the use of cash in some countries, whose currencies seem less attractive than the euro, there is no such trend away from cash in the euro area. Some 76% of all transactions in the euro area are carried out in cash, amounting to more than half of the total value of all payments. The demand for cash in the euro area currently outstrips the rate of nominal GDP growth. In crisis times, the demand for cash surges even higher. At mid-March this year, the weekly increase in the value of banknotes in circulation almost reached the historical peak of €19 billion.”

“The ECB’s debate on CBDCs is therefore mainly analytical.” adds Mersch. Whether and when it becomes more of a policy debate will largely depend on the preferences of households. He compares this to the choice of paperSee Banknote paper. More or polymerA substrate used in the printing of banknotes, made of biaxially oriented polypropylene (BOPP) polymer. Polymer banknotes were first introduced in Australia and are widely used around the world. More for banknoteA banknote (or ‘bill’ as it is often referred to in the US) is a type of negotiable promissory note, issued by a bank or other licensed authority, payable to the bearer on demand. More substrates, which the central bank would happily accommodate if people voiced a preference.

A retail CBDC, accessible to all, would be a game changer

Although there is not a concrete “business case” for a CBDC right now, that won’t stop the ECB “from seriously exploring the optimal design.” A wholesale model, restricted to a limited group of financial counterparties, would be largely business as usual. However, a retail CBDC, accessible to all, would be a game changer. “So a retail CBDC is now our main focus.” says Mersch.

He also stresses that a number of challenges remain unresolved at this point:

- Legal tenderMoney that is legally valid for the payment of debts and must be accepted for that purpose when offered. Each jurisdiction determines what is legal tender, but essentially it is anything which when offered (“tendered”) in payment of a debt extinguishes the debt. There is no obligation on the creditor to accept the tendered payment, but the act of tendering the payment in legal tender discharges the debt. More: should the CBDC have the same legal tender status as notes and coins?

- Anonymity: what level of anonymity would be provided and how can it be guaranteed?

- Disintermediation: if the central bank were to hold retail deposits, this could create a major disruption for the financial sector.

“These potentially highly adverse effects on the financial system would appear to outweigh the benefits envisaged by the introduction of a retail CBDC.” says Mersch.

This post is also available in:

![]()