The European Commission Considers Cash Payment Limitations Again

Chair, CashEssentials

This post is also available in:

![]()

The European Commission plans to introduce a cashMoney in physical form such as banknotes and coins. More paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More limitation of €10,000 across the European Union, said Financial Services Commissioner Mairead McGuiness in an interview with Süddeutsche Zeitung. “We’re talking about an upper limit of 10,000 euros. Carrying that much moneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More in your pockets is pretty difficult. Most people don’t do that. But we respect that citizens like cash, and we don’t want to abolish it.” said McGuiness.

In December 2020, the Commission published the summary of a public consultation of its action plan on money laundering and found that 73% of operators in the financial sector but only 46% of operators in the non-financial sector support introducing ceilings for large cash payments.

In 2018, the European Commission Decided not to Impose Limitations

In 2018, after a two-year consultation, the European Commission decided not to impose EU-wide limitations on cash payments. The Commission concluded in a report on the impacts of restrictions on payments in cash that “While tax fraud and the use of cash are often associated, the study demonstrates that the relationship between the two is not always clear-cut.”

The European Commission Recommendation 2010/191/EU states that the acceptance of payments in cash should be the rule but acknowledges that cash may be refused for reasons related to the ‘good faith principle,’ without this constituting a breach of the legal tenderMoney that is legally valid for the payment of debts and must be accepted for that purpose when offered. Each jurisdiction determines what is legal tender, but essentially it is anything which when offered (“tendered”) in payment of a debt extinguishes the debt. There is no obligation on the creditor to accept the tendered payment, but the act of tendering the payment in legal tender discharges the debt. More status of cash. The report adds: “[…] the impact of a cash restriction on money launderingThe operation of attempting to disguise a set of fraudulently or criminally obtained funds as legal, in operations undeclared to tax authorities, and therefore not subjected to taxation. Money laundering activities are strongly pursued by authorities and in most countries, there are strict rules for credit institutions to cooperate in the fight against money laundering operations, to declare and report any transactions that could be considered suspicious. More in general, cannot be precisely quantified. In this context, a declaration obligation would already provide law enforcement with intelligence”. It is not clear why the situation is different today.

Due Diligence Rules Are Already in Place

The European Anti-Money Laundering and terrorist financing rules already require that businesses and individuals take due diligence measures when receiving more than €10,000 in cash. This includes identifying and verifying the identity of the customer as well as the beneficial owner – that is, any person who ultimately owns or controls your customers or on whose behalf the transaction was conducted.

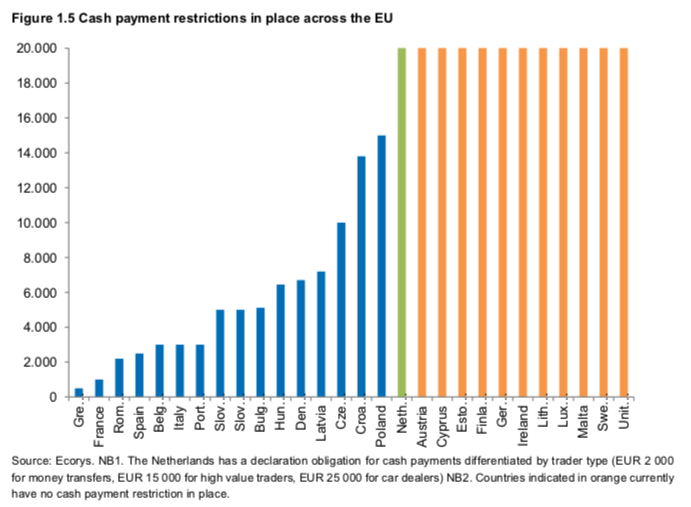

It is also noteworthy that 17 out of 27 Members States of the European Union have introduced cash payment limitations. The graph below shows that thresholds vary significantly, ranging from €500 in Greece to over €14,000 in Poland (Graph 1). In an EU wide-limitation of €10,000, 13 countries would actually see existing limitations increase.

17 Countries Already Have Limitations

Graph 1. European Union: Cash Payment Restrictions

In December 2020, a controversial law that would have banned cash payments over A$10,000 (approx. €6,348) had been voted out by the Australian Senate. Many saw it as infringing on the freedom to use cash and to protect one’s financial privacy.

This post is also available in:

![]()