Understanding the Cost of Payments

Chair, CashEssentials

This post is also available in:

![]()

During the Future of CashMoney in physical form such as banknotes and coins. More conference, CashEssentials hosted a research seminar on the cost of payments with presentations by the U.S. Federal Reserve, the Swiss National Bank (SNB), the Bundesbank, the European Central Bank (ECB) and the University of St. Gallen. While conclusions may differ, all papers highlighted the complexity of measuring the cost of payments.

Franz Seitz, from the Weiden Technical University of Applied Sciences and chair of the seminar, started by observing how little research there is into the cost of payments. Comparative studies are even rarer, with the 2019 52-country survey by Santiago Carbo-Valverde and Francisco Rodriguez-Fernandez being the exception. The complexity and cost of doing these studies appear to be the problem.

Understanding Business Behaviour

The SNB’s survey included a question to companies about why they accepted cash payments. The answer was that cash was significantly better than the alternatives in terms of cost and reliability compared with non-cash payments but worse regarding the risk of theft. In addition, they had to accept cash because customers needed and wanted to pay in cash.

It would be interesting to understand what was meant by ‘reliability’. Consumer behaviour can changeThis is the action by which certain banknotes and/or coins are exchanged for the same amount in banknotes/coins of a different face value, or unit value. See Exchange. More, and costs can vary. Still, if reliability were to tell assured paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More or resilience against software or power failures, this is a powerful positive for cash that is likely to remain. It would be interesting, as well, to ask businesses the same questions for non-cash payments, particularly around the risks of theft and crime.

The SNB asked businesses how they accessed cash, and one part of the answer said cash in transit (CIT) services were hardly used. Companies used their banks, post offices and customer cash-inflows/outflows to manage their cash.

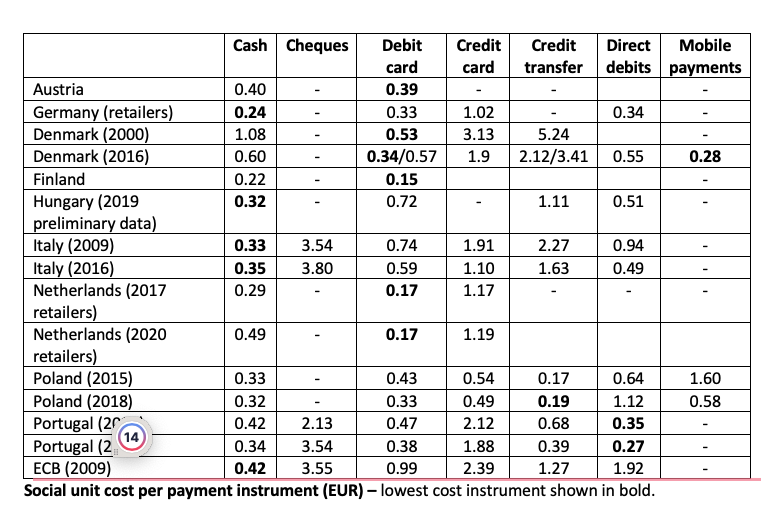

Societal Cost vs Private Costs

The ECB paper looked at nine cost-of-payment studies across Europe in recent years. They found that the payment environment was changing, driven by three elements – digitisation, regulatory change (Payment Services Directive 2, for example) and changing payment habits.

The ECB defined societal cost as the cost of providing payment services to society, coming from the resource costs incurred by all parties along the supply chain. Societal costs contrast with private costs, which are the costs incurred by individual stakeholders. If you regard cash as a public utility to be preserved, one might focus on private costs since this drives behaviour. A central bank, though, must consider the societal cost.

One challenge here is that powerful entities in the payment landscape have the market power to shape the behaviour of consumers, merchants and even banks. The societal cost, particularly in terms of consumer behaviour, does not just exist. Such ideas are hard to research and understand. The Bundesbank, for example, found that card costs are the most significant cost element for non-cash payments.

When the work of the nine studies was compared, cash was the most expensive means of payment in only one country: this was Finland, where cash volumes are low. In three countries, cash was always the lowest-cost instrument (Germany, Italy and Hungary), and overall cash was the lowest cost.

The work shows that when cash volumes are ‘high’, cash has the lowest societal impact per transaction: debit card fixed costs are high, so as their volumes rise, they become less expensive. The latter raises questions about whether central banks should support societal good by acting to maintain cash volumes.

Importance of Perceptions

Tobias Truetsch reported on research that showed that when the payment cost was visible to consumers, with the same price for all, people’s behaviour changed. The change was statistically significant, with people opting to use lower-cost payment means. The latter supports the case for requiring the cost of payments to be visible to allow proper consumer choice.

Final Word

The presenters were reporting on their studies, but the audience raised questions about the ability of commercial players to manipulate costs to further their interests, whether central banks could and should actively support cash volumes, whether requiring the cost of payments to be shown to consumers and whether the ‘reliability’ of cash is a fundamental strength.

This post is also available in:

![]()