As Payments Become more Digital, Bank of Finland Develops a Financial Literacy Programme

This post is also available in:

![]()

According to a 2016 OECD report, adults in many countries around the world display low levels of financial knowledge, fail to engage in financial behaviours that could improve their financial security and have financial attitudes oriented towards the short-term. The weakest areas of financial behaviour across these measures appear to be related to budgeting, planning ahead, choosing products and using independent advice. On average, across participating countries and economies, only 60% of adults reported having a household budget and only about 50% set long-term goals and tried to achieve them. In the report, Finland is ranked second in terms of overall levels of financial literacy.

“People no longer have such physical budget limitations as they used to do, and that makes it harder for people to manage their finances.”

Olli Rehn, Governor of the Bank of Finland

Yet, the Bank of Finland is designing a widespread financial literacy programme for its citizens aimed at reducing household debt. According to Bloomberg, household debt has almost doubled during the past twenty years and a record 7% of the population are unable to pay their bills. Low interest rates have clearly contributed to this situation. But the growing use of digital payments and the declining use of cashMoney in physical form such as banknotes and coins. More in transactions have also played a role in the loss of budget management skills. Olli Rehn, the Governor of the Bank of Finland, says, “Consumers have largely already moved to a digital world” when it comes to payments. “People no longer have such physical budget limitations as they used to do, and that makes it harder for people to manage their finances.”

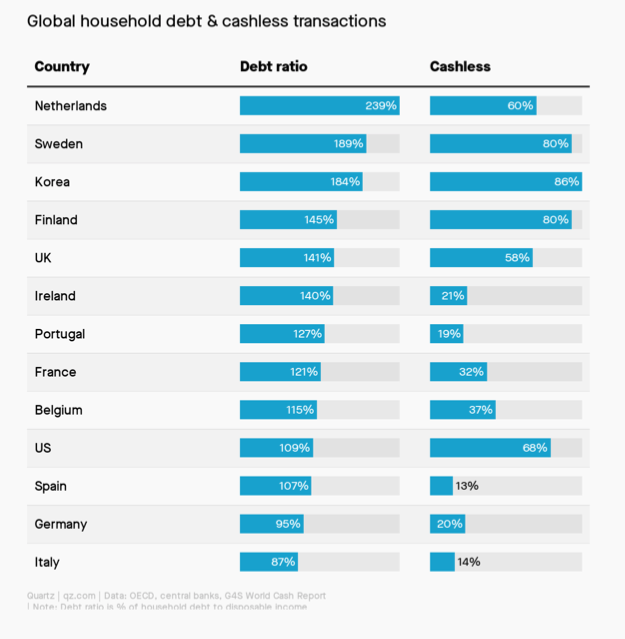

Less cash more debt?

The phenomenon is not limited to Finland. John Detrixhe, in Quartz establishes a correlation between household debt levels and the share of digital transactions.

The Global Financial Literacy Excellence Center concludes that “users of mobile payments are more likely to overdraw their checking accounts, use credit cards expensively, borrow through alternative financial services, and withdraw from their retirement accounts. Even after we control for socio-demographic factors, results continue to show that mobile paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More users are more likely to engage in behaviors that do not seem to follow good financial management practices.”

In Australia, the not-for-profit Financial Basics Foundation has concluded that students are also struggling with financial literacy. Results from a 2017 survey show that despite 85% believing that they have a good understanding of how credit works, their responses to some basic questions were off target. Donnel Briley, professor of marketing and behavioral psychology at Sydney University confirmed that “there’s good empirical evidence that people spend more moneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More when they don’t actually have to use cash, and that goes across different alternative forms of payment.”

The Bank of Finland’s programme is still under construction and is co-ordinated with the Ministry of Justice and other key authorities. Work will begin with an analysis of the current state of financial literacy in Finland, in cooperation with key researchers in the field. Next, the Bank of Finland and the other parties involved in the coordination work will map out the actors in the field of financial literacy and review ongoing activities and projects. Thereafter, a framework will be established, and a plan drawn up for national cooperation. The website already includes some challenging tests.

“Payment is a basic function of human society, and it essentially underlies all economic activity”

Tuomas Välimäki, Member of the Board of the Bank of Finland

Besides the financial literacy programme, the Bank of Finland has also outlined its cash services policy which is articulated around five guiding principles:

- Commercial banks are obligated to ensure their customers can make deposits to and withdrawals from their bank accounts.

- Customers are entitled the right to make a reasonable number of cash withdrawals from their account at no charge.

- Small businesses and associations should be viewed as private customers with regard to their use of cash services

- CashbackA service whereby the customer pays electronically a higher amount to a retailer than the value of the purchase for goods and/or services and receives the difference in cash. It is also a reward system associated with credit card usage, whereby the consumer receives a percentage of the amount spent on the credit card. More at stores should be available for all customers in a fair manner.

- Cash should be accepted at the very least as payment, in circumstances where citizens use services critical for their well-being.

This post is also available in:

![]()