“Bancaída:” Banking Platforms’ Outage in Colombia

Ph.D. in U.S. History, Columbia University in the City of New York

Post-Doctoral Researcher in Global Correspondent Banking, 1870-2000 – Mexico and South America, University of Oxford

This post is also available in:

![]()

La “Bancaída”

On December 1, a payday in Colombia, Davivienda, Bancolombia, and Nequi’s banking platforms went down. People could not withdraw cashMoney in physical form such as banknotes and coins. More from ATMs, pay with their cards at supermarkets, restaurants, and gas stations, or conduct operations in bank branches and apps.

Many users took to social media to complain about their banks’ faulty services, calling the meltdown the “Bancaída” (the bank fall).

“Davivienda and Bancolombia are always trending [topics] due to their BAD products Daviplata and Nequi, respectively/Shameful!” tweeted Sonia Cett (@sony_ca21).

Davivienda

Founded in 1972, Davivienda has 19.8 million clients, 17.8 thousand employees, 652 branches, and 2,670 ATMs. DaviPlata, its digital bank, has 15.6 million clients.

Starting at 8 am on December 1, Davivienda experienced problems with their website and app. The bank’s ATMs were not dispensing cash (see Image 1); clients could not use debit and credit cards. Davivienda branches could not handle operations.

“Today we had failures in some of our Davivienda and DaviPlata channels. Our IT team is working to solve these issues. Our ATM network and our branches are fully functional for Davivienda clients needing cash. Clients needing to use other paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More instruments can use their credit cards at retailers without problems. […] This situation did not arise from an attack or a vulnerability in the bank’s infrastructure,” said Davivienda.

Image 1. Colombia: Davivienda ATMs Shut Down, 2022

Source: @MaicolBuitrago, @Paamogar.

Bancolombia

Founded in 1875, Bancolombia has 25 million clients, 30,000 employees, 878 branches, and 6,050 ATMs. Bancolombia’s services went down on December 1 and again on December 10. Clients could “get cash through our banking correspondents and ATMs, and use their cards,” tweeted Bancolombia.

Nequi

Launched in 2015 as Bancolombia’s digital bank, Nequi has 14.6 million customers. After Bancolombia spun it off in December 2021, Nequi started providing loans to customers purchasing flight tickets (via Hopper) and receiving remittancesMoney sent home from emigrants working abroad. More (via Ria MoneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More Transfer).

“We have identified a faulty module and are implementing an action plan to solve it with teams in Colombia, the United States, and Brazil. However, this is a complex process. [… Failures] are not related to scalability due to transactions’ growth or volume, or Nequi’s independence from Bancolombia,” said Nequi.

Nequi said it gave free payment cards to its worst affected customers. Nequi’s app failed again on December 7. “As soon as we solve [the situation], you will be able to use Nequi and move your money as usual. […] For now, the Nequi card works perfectly,” said Nequi in a deleted tweet.

Health Provider Experiences Cyberattack

At first, some suspected hackers were attacking the banks.

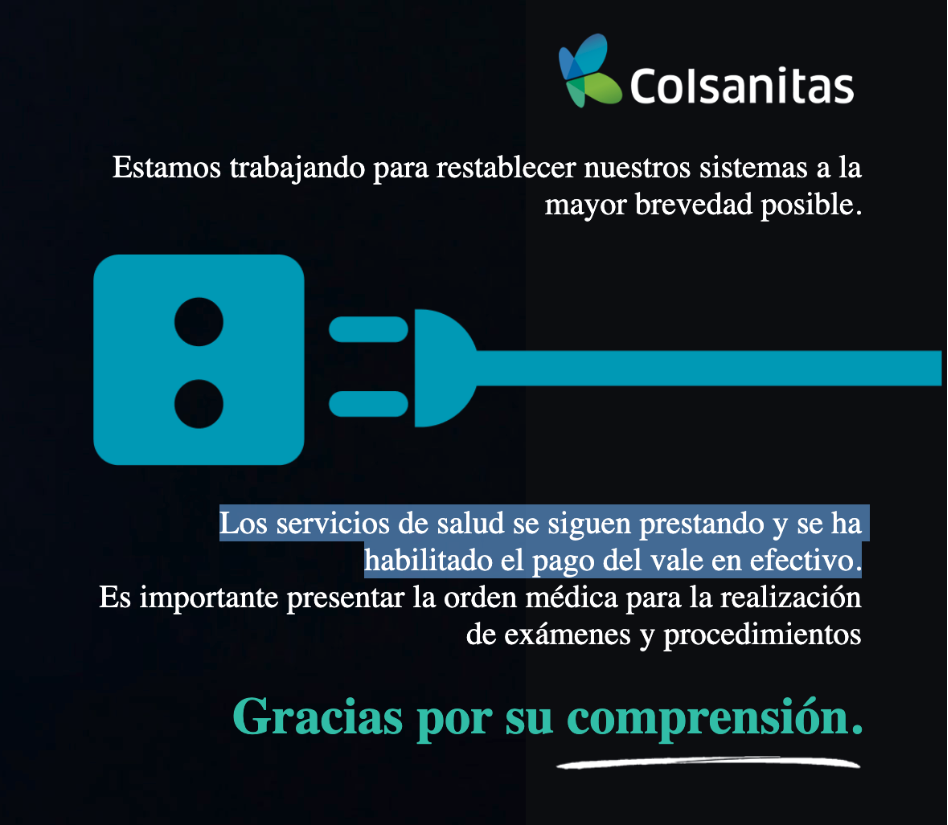

- On November 29, Keralty, a medical consortium owned by Colsanitas, reported having faced a cyberattack. Sanitas’ website was unavailable for several days. Later, its home page showed the legendRefers to the lettering, words or phrases that are engraved on coins, usually located along or around the outside edge of the coins. More, “We continue providing health services, and have enabled cash payments” (see Image 2).

- OmegaPro, an online forex investing firm, was the victim of a “sustained and sophisticated cyberattack by an unknown organized criminal group.” OmegaPro users cannot withdraw their funds from the platform.

Image 2. Colsanitas: We Take Cash, 2022

Source: Carlos León.

SEMANA and Portafolio contacted the police’s cybercrime unit to inquire whether Davivienda, Bancolombia, and Nequi were suffering cyberattacks. The police stated it had no reports of hacking, indicating that the “Bancaída” was due to the banks’ systems.

- “For now, the banks have not reported a cyberattack,” said the director of security and operations of Asobancaria, the Colombian banking association. Notably, Asobancaria’s website seems to have been hacked, as several pages (such as its About section) redirect here.

- “We activated our protocols and saw that the failure of banking services and the digital platforms of Davivienda, Bancolombia and Nequi were platform issues, not cyberattacks. In the case of the Sanitas health provider owned by the Keralty group, we are waiting for the company’s report,” said Sandra Urrutia, the Colombian minister for IT and communications.

- “Without evidence of the reason for the system downtime it is difficult to link it to a cyberattack, but currently when a company’s systems are down, it is logical to think first it is under attack, even if it is not true because of the number of cyberattacks that are occurring,” said Fabio Assolini, director of the Global Research and Analysis Team for Latin America at Kaspersky.

The Resilience of Cash vs. the Vulnerability of Digital Infrastructures

Colombia’s “Bancaída” is another example of what happens when digital infrastructures fail due to outages (such as the Rogers’ outage in Canada last July) or cyberattacks (like the January and February attacks against Ukraine) and the importance of preserving cash as a resilient payment instrumentDevice, tool, procedure or system used to make a transaction or settle a debt. More.

- “This is a good reminder of how important it is to preserve cash. Cash is resilient. Cash grants much needed redundancy to the payment system and makes it less fragile to operational outages. Going cash free does not make the society better. It makes it worse for everyone—but gives profits to a few that use the argument of financial inclusionA process by which individuals and businesses can access appropriate, affordable, and timely financial products and services. These include banking, loan, equity, and insurance products. While it is recognised that not all individuals need or want financial services, the goal of financial inclusion is to remove all barriers, both supply side and demand side. Supply side barriers stem from financial institutions themselves. They often indicate poor financial infrastructure, and include lack of ne... More. Reducing our payment options and forcing us to abandon a resilient payment instrument is not progress,“ wrote Carlos León, financial market infrastructures & digital currencies solutions director at FNA.

This post is also available in:

![]()