Public Discourse on Cash

In a recent paperSee Banknote paper. More Public Discourse on Retail Payments and the Case of CBDC (SAFESecure container for storing money and valuables, with high resistance to breaking and entering. More Working Paper No. 474, April 2026), Ulrich Bindseil [1], former Director General of Market Infrastructure and Payments at the European Central Bank, analyses how stakeholders in the retail payments industry shape public debates and policymaking. His focus is primarily on digital payments, particularly CBDCs, which he argues have triggered unprecedented public debate. Notably, while central banks’ mandate to issue cashMoney in physical form such as banknotes and coins. More is acknowledged, the broader discussion on the role of cash in retail payments is largely omitted.

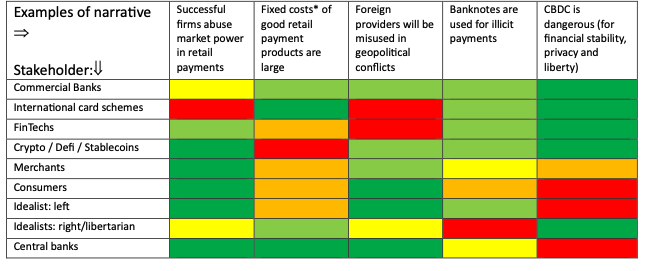

Bindseil’s analysis reveals a heat map of stakeholder positions on key narratives. For example, the claim that CBDCs are dangerous (for financial stability, privacy, or liberty) is supported by the payments industry (banks, card schemes, fintechs, and the crypto community) but rejected by merchants, consumers, left-leaning idealists, and central banks. Conversely, the argument that banknotes enable illicit activities is backed by the industry’s supply side—yet opposed by consumers and right-wing libertarians. Central banks remain neutral on this narrative, the only instance where they take no stance.

Heat map – examples of views of key retail payments stakeholders on selected narratives

Source: Bindseil U. Public Discourse on Retail Payments and the Case of CBDC (SAFE Working Paper No. 474, April 2026)

Bindseil highlights the difficulty of crafting clear, coherent messages when stakeholders hold divergent priorities, definitions, and even terminologies. The public discourse on cash faces identical challenges. As digital payments and new forms of money—CBDCs, stablecoins, and commercial bank money—compete for dominance, cash has become a polarizing topic, with fragmented narratives pulling it between security and liberty, efficiency and inclusivity, tradition and progress.

From Retail Payments to Cash

Bindseil identifies three core challenges in the public discourse on retail payments:

- Competing Frames: Stakeholders emphasize conflicting aspects—stability, innovation, or equity—without engaging with each other’s concerns.

- Technical vs. Social Divides: Experts focus on efficiency and risk, while the public debates trust, autonomy, and fairness.

- Rapid ChangeThis is the action by which certain banknotes and/or coins are exchanged for the same amount in banknotes/coins of a different face value, or unit value. See Exchange. More: Innovation outpaces institutions’ ability to communicate its implications clearly.

These challenges mirror those facing cash. Just as central banks struggle to explain their role amid fintech and digital currencies, the discourse on cash is torn between security and privacy, technical efficiency and social value. Applying Bindseil’s framework helps explain why messages about cash often miss their mark—and how to improve them.

The Fragmentation of Cash Narratives

Competing Frames: Misaligned Priorities

Stakeholders emphasize different dimensions of cash without addressing each other’s core concerns. Some politiciansand financial institutions frame cash as a risk to security and transparency, citing its role in illicit activities and advocating for digital alternatives. Meanwhile, privacy advocates argue that cash protects individual freedoms, framing restrictions as overreach. The result is a debate where the same facts support opposing conclusions, with little effort to reconcile perspectives.

The Technical vs. Social Divide

Technocrats discuss cash in terms of cost, scalability, and efficiency, portraying it as an inefficiency to be minimized. Yet this overlooks its social and cultural significance: for many, cash is a symbol of trust, a budgeting tool, and a lifeline for the unbanked. The COVID-19 pandemic underscored this, as demand for physical cash surged amid uncertainty. A discourse focused solely on technical metrics risks alienating those who see cash as a social contract—one guaranteeing access, universality, and resilience.

Analogue vs. Digital: The Innovation Paradox

Digital currencies are often presented as the inevitable future, rendering cash an outdated relic. Yet this framing ignores the unique attributes of cash: offline functionality, universality, and its role as interest-free central bank moneyA liability of a central bank, including banknotes in circulation and banks’ deposits with the central bank. More. The discourse often fails to recognize that cash and digital moneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More are not mutually exclusive. A diversified monetary ecosystem—embracing both—offers greater resilience and inclusivity than a digital-only system.

Toward a Coherent Discourse on Cash

Embrace Nuance, Reject Binaries

Cash is neither wholly good nor bad; its value depends on context. A nuanced discourse acknowledges the legitimacy of both security and privacy concerns, as well as efficiency and inclusivity. Instead of pitting cash against digital, we should explore how they complement each other—cash as a fallback, a tool for inclusion, and a check on digital monopolies.

Develop a Shared Vocabulary

A shared terminology is essential. Clear, consistent definitions of terms like “public good,” “financial inclusionA process by which individuals and businesses can access appropriate, affordable, and timely financial products and services. These include banking, loan, equity, and insurance products. While it is recognised that not all individuals need or want financial services, the goal of financial inclusion is to remove all barriers, both supply side and demand side. Supply side barriers stem from financial institutions themselves. They often indicate poor financial infrastructure, and include lack of ne... More,” and “cash” can align stakeholders. Defining cash as accessible, offline, interest-free central bank money could provide a foundation for coherent messaging.

Bridge the Silos

The discourse on cash must become interdisciplinary, bringing together economists, sociologists, technologists, lawyers and civil society. Collaborative forums are needed to foster cross-sector dialogue and develop a holistic understanding of cash’s role.

Ground the Discourse in Evidence

Evidence-based communication requires data not only on cash usage and costs but also on its social and cultural significance. Research on why people value cash—beyond its technical properties—can inform more inclusive policies. For example, studies on the impact of cash restrictions on vulnerable populations can highlight the human stakes of policy decisions.

Adopt a Forward-Looking Perspective

Stakeholders should proactively shape the future of money, discussing how cash can coexist with digital payments, be integrated into hybrid systems, and preserve its unique properties in a digital world. The discourse must move beyond defence to vision, articulating a positive, evolving role for cash.

Prioritize Public Engagement

Public trust is paramount. The discourse on cash must prioritize public engagement, ensuring citizens’ voices shape its future. Consultations, surveys, and open forums can help understand public values and concerns. After all, given the public good attributes of cash, its future should reflect the needs of those it serves.

The Path Forward

The public discourse on cash stands at a crossroads. The fragmentation—competing frames, technical vs. social divides, and rapid change—mirrors the obstacles Bindseil identifies in retail payments debates. Yet his lessons offer a roadmap for a more coherent conversation.

By embracing nuance, developing shared terminology, bridging silos, grounding the discourse in evidence, adopting a forward-looking perspective, and prioritizing public engagement, we can craft a unified message about cash. In an era of intensifying competition between payments and forms of money, the future of cash depends not only on its technical properties but on our ability to discuss it clearly, collaboratively, and compellingly.”

Bindseil concludes “Legislators and central banks should have capacity for independent economic analysis and producing empirical evidence when evaluating retail paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More policy options.” This applies to cash as well.

.

[1] I would like to thank Ulrich Bindseil for comments.