Why Retailers Juggle Debit and Credit Cards and Cash?

This article is republished from The Conversation in French under a Creative Commons licence. The translation is by CashEssentials.

Paying at the till is an ordinary, routine activity. But who really decides how we pay in small shops in France? To answer these questions, I conducted an ethnographic study among shopkeepers and customers, interviewing them about their transactions in numerous small shops in both the Île-de-France region and the Toulouse metropolitan area, in Haute-Garonne.

We are more familiar with the use of moneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More within households – pocket money for instance but less so with how people pay in shops.

This is why our research sheds light on paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More in small shops, focusing on the balance between cashMoney in physical form such as banknotes and coins. More and digital money.

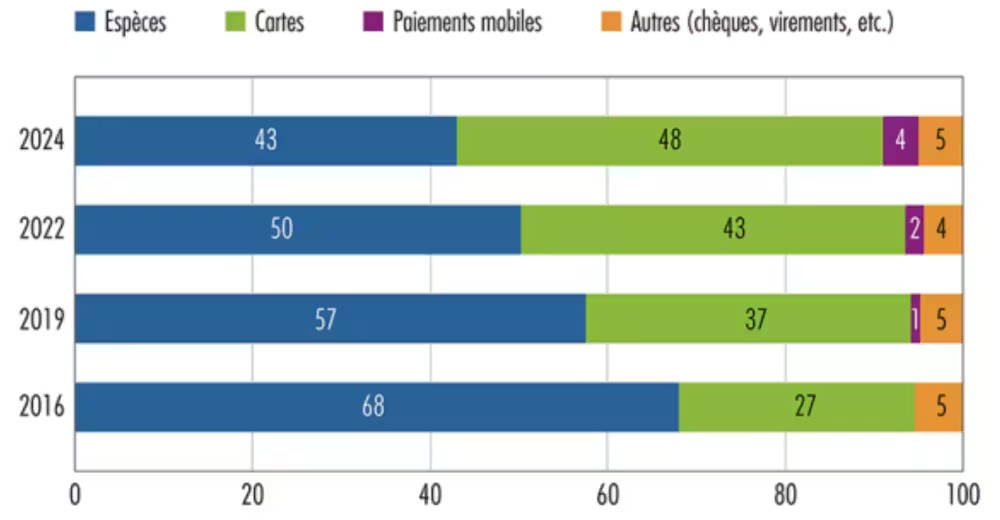

Cash less Widely used than Bank Cards

The use of cash is declining in favour of digital payments, particularly since the post-pandemic period following Covid-19. For the first time, the Banque de France has announced that, in 2024, cash was used less than bank cards.

Mix of Payment Instruments by Volume at the Point-of-Sale in France

Source: Banque de France

Accepting cash is a legal obligation in France, ensuring there is no discrimination against cash payments. Within these constraints, retailers in France are free to choose the payment methods they accept, to set the authorised limit for card payments, and to refuse or accept payments by cheque and meal vouchers in the hospitality industry, with a few exceptions, such as the requirement for taxis accept cards as part of the fight against value-added tax (VAT).

Yet professionals rarely have the opportunity to work autonomously:

“Everyone pays by card! People can’t be bothered to go and get cash anymore. They don’t carry any cash on them these days,” says the manager of a bakery.

From Bank Cards to Bitcoin

In practice, digital payments (mainly by card) are the most common method of payment. Far from being equipped with the state-of-the-art technology found in large retail chains – self-service checkouts, ordering terminals or unstaffed checkouts – shopkeepers nonetheless cultivate their skills of observation and intuition, which are characteristic of the world of very small businesses, to reassess their sales processes: they invest in up to two, and sometimes three or four, point-of-sale terminals so that sales staff can handle transactions without assistance.

Nearly 88 per centFraction of a currency representing the hundredth of the unit of account. More of shopkeepers I spoke to (in 69 shops) are equipped with card payment terminals to streamline the checkout process, particularly at peak hours. The value of the transaction also influences behaviour towards the use of digital money:

“ For amounts above €30, it’s uncommon for them to pay in cash”, points out an employee at a hairdressing salon.

New payment methods, such as BitcoinBitcoin is commonly said to be a cryptocurrency, a digital means of exchange developed by a set of anonymous authors under the pseudonym of Satoshi Nakamoto, which began operating in 2009 as a community project (Wikipedia type), without the relationship or dependency of any government, state, company or body, and whose value (formed by a complicated system of mathematical algorithms and cryptography) is not supported by any central bank or authority. Bitcoins are essentially accounting entries i... More, are rarely accepted by small shops, with the exception of ‘Bitcoin Street’ in the capital, a sign of low uptake as a payment methodSee Payment instrument. More amongst customers.

Getting rid of ‘the Dirty Work’

Just as cashierInitially, the person who is responsible for the safe, its opening and closing, and the contents that are safeguarded inside it. Nowadays, at a central bank, the person who is responsible for matters related to the treasury and cash. Their signature would usually appear alongside others on the banknotes issued by the bank. More duties are among the tasks considered by sales assistants to be the least interesting in department stores, cash-accepting devices and digital payment methods are emerging in small shops with high sales volumes as tools to get rid of “the dirty work” associated with handling cash.

Small shops are inclusive meeting places, as explained by American sociologist Ray Oldenburg. Most of them emphasise the importance of cash, as a public good that must be protected and regulated by institutions:

“We have a lot of customers here who pay in cash. It would be a real problem for these people if there were no more cash,” explains the manager of a tobacconist.

Cash-accepting devices streamline cash-handing. Photo credits: Aude Danieli, courtesy of the author.

Far from all the talk of the ‘cashless society’ – or, to put it plainly, a society without cash – and the digitisation of money, the process of digitisation is far from complete. Cash is still used on a daily basis. In the local markets of working-class neighbourhoods, paying in cash is the social norm and (often) serves as a means of haggling.

In affluent neighbourhoods, cash is far from having disappeared, but it usually accounts for less than 20 per cent of takings, according to estimates from the professionals interviewed. For some, however, handling cash provides tangible proof of the transaction: ‘I like to feel it in my hand,’ explains an employee at a bakery.

Accepting the Local Rules of the Game

Generally speaking, small shopkeepers do not seek to nudge customers towards the payment methods they consider most advantageous. Why is this?

Business owners are bound by the dynamics of commercial exchangeThe Eurosystem comprises the European Central Bank and the national central banks of those countries that have adopted the euro. More to be ‘good shopkeepers’ who play by the neighbourhood’s rules:

‘Payment card fees are expensive, but it’s the meal vouchers that really take the pinch! We lose 20 per cent (…) [but] we can’t refuse them,’ says the manager of a bistro-restaurant.

Whilst payment cards make it easier to track spending, cash helps to maintain secrecy and conceal transactions. Our study highlights a significant number of precautions and preconceived judgements regarding cash:

“If they pull out a payment card, I get my card machine out. It’s an exchange. I’m not going to say to them: ‘Why aren’t you paying in cash?’” That makes me look like a stingy old man,” recalls the manager of a home décor shop.

“No Payments Cards for Amounts Under 1 euro”

In an attempt to carve out areas of resistance, business owners have been trying to influence the use of payment methods. They set minimum thresholds for card payments, or they simply don’t bring out the card terminal – a practice observed at markets – in order to boost cash takings.

Setting minimum thresholds for card payments helps businesses cope with the long-standing costs of digitising payments. Another practice, though rare and extreme, involves outright refusing card payments:

“My accountant gave me an estimate: I’d save between € 30,000 and 60,000 by refusing card payments!” recalls the manager of a bar-restaurant.

These business practices to nudge customers towards a particular payment method are reflected in a multitude of payment signs designed to pre-empt any customer dissatisfaction: ‘We no longer accept cheques’, ‘Cards accepted for amounts over 5 euros’, ‘No credit cards!’

Even before reaching the till, customers must, of course, carry the correct means of payment.

Many shops do not accept credit cards for amounts below a certain threshold. Aude Danieli, Courtesy of the author

Changing the usual Customer-Merchant Relationship

Payment is paired with small gestures and negotiations. Rounding off prices and offering discounts – ranging from a few cents to several tens of cents – are commonplace at food stalls -are driven by a desire to satisfy customers (both regulars and potential new customers):

‘Good customers like this lady – if it’s € 7.40, I’ll round it down to 7. I round off small amounts. It’s really odd. If you round it up – say to 10, 15, 20, 30, 40 or 70 cents – they’re happy […]: 70 cents is nothing! ”, points out a cheesemonger.

The moment of payment is sometimes the opportunity for jokes to maintain the customer relationship, a practice often seen at markets and in the bar and restaurant sector:

“Sometimes I joke by saying: ‘I’ll even accept metro tickets, transit cards and meal vouchers.’ “But no, I don’t accept them because I’m not in the food trade,” notes a manager of a home linen stall at the markets, with a touch of irony.

Wordplay and forms of interaction “break the usual commercial rapport” so familiar in open-air markets. But the moment of “payment” remains precarious. A saleswoman in the wine trade testifies to this:

“It stresses me out. Until the card terminal has registered the amount, I don’t know if the transaction has actually gone through.”

Eliminating the Act of Payment

Cash lends itself more readily to discounts and tips; credit cards, on the other hand, are subject to usage rules that make the commercial relationship more rigid.

‘The fare is € 53. The customer gives me a 50 note – well, he doesn’t have the 3 euros, so I’ll let him off. With a card… it’s not possible to give discounts. If the taxi meter reads 7.30 and you ask for 7 euros, the invoice takes precedence – I have to charge VAT on the invoice,” explains the manager of a taxi company.

Cash remains commonly use in local markets. Photo credit Aude Danieli, Courtesy of the author

When you pay at your local shop, the shopkeeper must juggle with various payment methods – such as cash or meal vouchers – while dealing with customers, who are sometimes impatient, and maintaining the standards of customer service expected in a local shop.

Payment signs and electronic payment infrastructure – particularly with the rise of contactless payments and cash-accepting machines – reveal another player in this retailer-customer relationship: payment intermediaries (VISA transaction networks, Sumup payment terminals, etc.) and, in the background, the discreet attempts within the Fintech sector to reinvent or even try to do away with the act of payment altogether.