US Payment Trends: The Unwavering Relevance of Cash

Key Findings

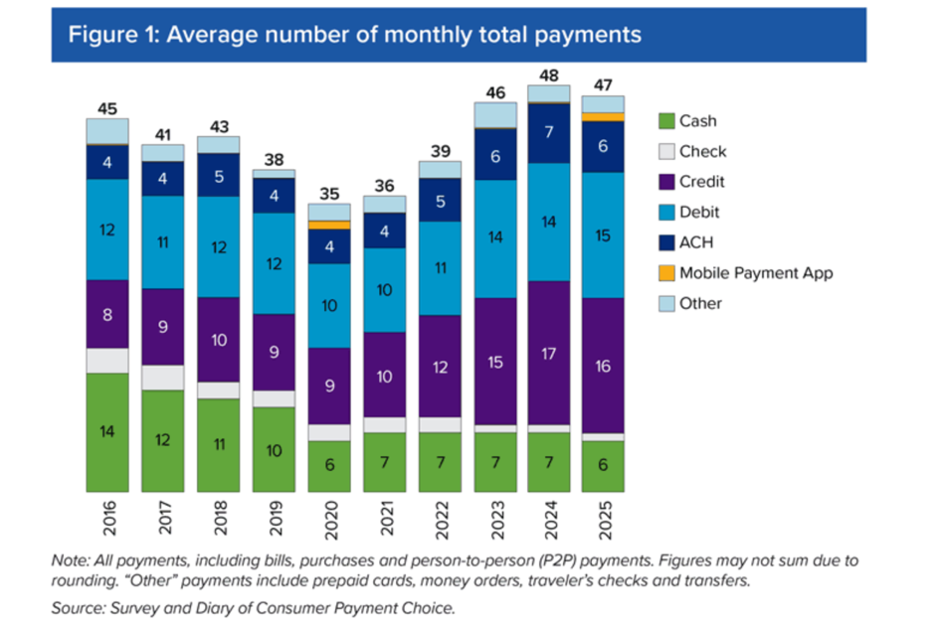

- CashMoney in physical form such as banknotes and coins. More remains the third-most-used payment methodSee Payment instrument. More in the U.S., accounting for 14% of all consumer payments in 2025.

- Consumers made an average of seven cash payments per month in 2025, stable since 2020, reflecting its persistent role.

- Nearly 80% of consumers carried cash daily in 2025, with an average holding of $67, underscoring its reliability.

- Cash serves as a primary paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More method for lower-income and older adults, while younger consumers prefer digital payments.

- More than 90% of consumers plan to continue using cash, highlighting its ongoing relevance as a payment method and store of valueOne of the functions of money or more generally of any asset that can be saved and exchanged at a later time without loss of its purchasing power. See also Precautionary Holdings. More.

Cash remains a vital and irreplaceable component of the U.S. financial ecosystem. The rise of digital paymentshas transformed consumer transactions, yet cash persists as a primary payment method for many, a reliable backup during system failures, and a crucial store of value in uncertain times. The Federal Reserve’s 2025 Findings from the Diary of Consumer Payment Choice by Shaun O’Brien and Hailey Phelps highlights how the unique attributes of cash—anonymity, near-universal acceptance, and minimal transactional costs—ensure its enduring relevance.

The Persistent Role of Cash as a Primary Payment Method

Cash remains the third-most-used payment instrumentDevice, tool, procedure or system used to make a transaction or settle a debt. More in the U.S., following credit and debit cards. In 2024, consumers made an average of seven cash payments per month, a figure unchanged since 2020. This stability underscores it’s enduring role as a primary payment method for many consumers, particularly those who prefer tangible currencyThe money used in a particular country at a particular time, like dollar, yen, euro, etc., consisting of banknotes and coins, that does not require endorsement as a medium of exchange. More for daily transactions.

Cash is especially important for certain demographics. Households earning less than $25,000 per year and adults aged 55 and older rely more heavily on cash than other cohorts. These groups often have limited access to digital payment infrastructure or prefer the simplicity and reliability of cash transactions. This demographic trend highlights cash’s critical role in ensuring financial inclusionA process by which individuals and businesses can access appropriate, affordable, and timely financial products and services. These include banking, loan, equity, and insurance products. While it is recognised that not all individuals need or want financial services, the goal of financial inclusion is to remove all barriers, both supply side and demand side. Supply side barriers stem from financial institutions themselves. They often indicate poor financial infrastructure, and include lack of ne... More and accessibility.

Cash as a Reliable Backup Payment Option

Cash serves as a crucial backup payment option, particularly during digital payment system failures or in areas with limited connectivity. The Federal Reserve emphasizes the role of cash in times of crisis and business disruption, ensuring that consumers have access to a reliable payment method when digital systems may be unavailable. This reliability is essential for maintaining consumer confidence in the U.S. payment system..

Nearly 80% of consumers carried cash daily in 2025, with an average cash holding of $67. This widespread behaviour reflects consumers’ trust in cash as a readily available and reliable payment option. The average amount of on-person cash was $67 in 2024, a slight decrease from $74 in 2023 but greater than in 2019. This indicates a consistent trend of consumers carrying more cash than before the pandemic, reflecting ongoing concerns about financial security and the need for readily available funds.

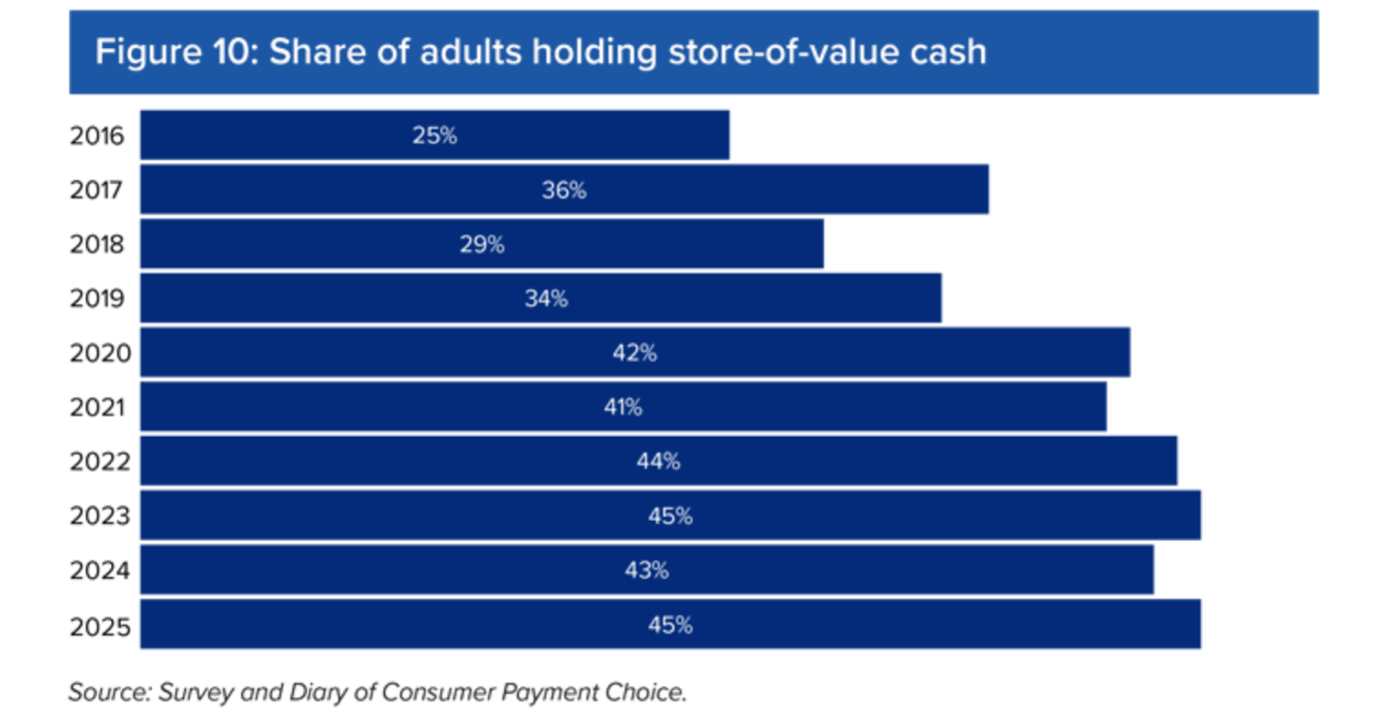

Cash as a Store of Value in Times of Uncertainty

The role of cash as a store of value remains critical, especially in times of economic uncertainty. Store-of-value holdings have remained elevated compared to pre-pandemic levels. These holdings reached $364 in 2025 up from $306 in 2024. This trend suggests that consumers have maintained higher cash holdings as a precautionary measure, likely influenced by economic uncertainty and the need for financial security. The tangible nature of cash provides a sense of security and control that digital currencies and electronic payments may not fully replicate.

Unique Advantages of Cash: Anonymity, Acceptance, and Cost

Cash transactions offer anonymity, a feature highly valued by privacy-conscious individuals. Unlike digital payments, which leave electronic trails and require personal data, cash allows users to conduct transactions without exposing personal information. This anonymity reduces risks of data breaches and identity theft, making cash a preferred payment method for those concerned about privacy.

Near-Universal Acceptance

Cash is accepted nearly everywhere, from large retailers to small businesses and informal markets. This universal acceptance ensures that anyone, regardless of access to technology or banking services, can use cash. In contrast, digital payments require infrastructure such as internet connectivity, POSAbbreviation for “point of sale”. See Point-of-Sale terminal. More terminals, and bank accounts, which are not universally available. This widespread acceptance makes cash a crucial payment method for ensuring financial inclusion.

Minimal Transactional Costs

Cash transactions incur minimal costs compared to digital payments, which often involve interchange fees, processing fees, and potential surcharges. For small businesses and low-income consumers, these costs can be significant, making cash a more economical choice. The survey suggest that while there are characteristics of cards that consumers prefer over those of cash, consumers previously identified cash as the least costly payment instrument.

The Complementary Relationship Between Cash and Digital Payments

The Federal Reserve’s role in ensuring the availability of cash, especially during times of crisis and business disruption, highlights the importance of cash as a backup payment option and a store of value. This complementary relationship between cash and digital payments ensures a resilient payment ecosystem that can adapt to various consumer needs and economic conditions.

The survey reveals that cash usage has remained stable. This stability suggests that cash continues to fulfill unique functions that digital alternatives have yet to fully replicate, particularly in its anonymity, near-universal acceptance, and minimal transactional costs.

“Cash continues to play an important role in the evolution of the payments ecosystem, serving as a primary instrument for some, a reliable backup option for others, and an increasingly important role as a store of value for many. The persistence of cash across these roles, combined with the significant majority of consumers planning to use cash in coming years, suggests that cash fulfills functions that digital alternatives have yet to replicate, particularly in its anonymity, near-universal acceptance and minimal transactional costs.” conclude co-authors Shaun O’Brien and Hailey Phelps.