Swiss payments service provider identifies future scenarios of money and crashes

This post is also available in:

![]()

Six is a provider of infrastructure and digital services for the financial services industry based in Switzerland. Amongst other activities, Six processes card payments in Switzerland and in other European countries and also manages the ATM network in Switzerland and Liechtenstein, connecting over 6,000 devices.

As part of its R&D effort, Six has published a white paperSee Banknote paper. More entitled The Future of MoneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More which proposes possible scenarios for money, including cashMoney in physical form such as banknotes and coins. More and digital forms within a 5 to 7 year horizon. The scenario-planning exercise analyses a range of factors – social, technological, economic, environmental and political – which will likely influence the future of money. The data is used to project seven possible scenarios, which are then ranked in terms of likelihood. The scenarios are summarized in the chart below.

Source: Six

As shown in the chart above, the level of cash usage is a key factor in the seven scenarios. And all scenarios foresee a decline in cash usage but only one sees it disappear altogether.

In the first – and most likely – scenario the decline in cash demand is predicted to reach 40-60% whereas the use of cash as a payment instrumentDevice, tool, procedure or system used to make a transaction or settle a debt. More would drop by 40-70%. In the second scenario, cash demand would decline by 80%, as “people may continue to hold cash as a back-up means of paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More for blackout and network interruption events.”

The third scenario envisages the adoption of a Central Bank Digital CurrencyThe money used in a particular country at a particular time, like dollar, yen, euro, etc., consisting of banknotes and coins, that does not require endorsement as a medium of exchange. More. The impact on cash demand is unclear: people may continue to use cash for privacy reasons and to avoid negative interest rates.

The fourth scenario would see the emergence of private digital currencies and the disappearance of central banks and sovereign currencies altogether. However, it is noteworthy that this scenario envisages that new money issuers could develop physical forms of money and leverage the existing cash infrastructure.

The fifth scenario would see cash disappear altogether. Governments would not only withdraw cash from circulation but would also prohibit the issuance and usage of alternative forms of physical currency, including foreign currencies.

In the sixth scenario, there is no money, physical or digital; no asset is recognized as fulfilling the three functions of money – store of valueOne of the functions of money or more generally of any asset that can be saved and exchanged at a later time without loss of its purchasing power. See also Precautionary Holdings. More, transaction instrument and unit of account. A barter economy would function driven by algorithms, artificial intelligence and the use of digital rights.

The seventh scenario envisages the widespread adoption of crypto-currencies such as BitcoinBitcoin is commonly said to be a cryptocurrency, a digital means of exchange developed by a set of anonymous authors under the pseudonym of Satoshi Nakamoto, which began operating in 2009 as a community project (Wikipedia type), without the relationship or dependency of any government, state, company or body, and whose value (formed by a complicated system of mathematical algorithms and cryptography) is not supported by any central bank or authority. Bitcoins are essentially accounting entries i... More or Ether as people lose trust in their governments. In this case, cash may co-exist if it is linked to crypto-coins.

The transition to a cashless society is much heralded, but is it really inevitable or desired?

The narratives that cash demand will decline or that cash will disappear altogether are not uncommon, especially when presented by digital payment providers. A recent Ernst and Young white paper, entitled “The end of cash: why when and how to flick the switch” raises the question: “The transition to a cashless society is much heralded, but is it really inevitable or desired?” However, the Six White Paper fails to emphasize to what extent even the most likely scenario – based on a ‘slow’ decline in cash demand would represent a major disruption.

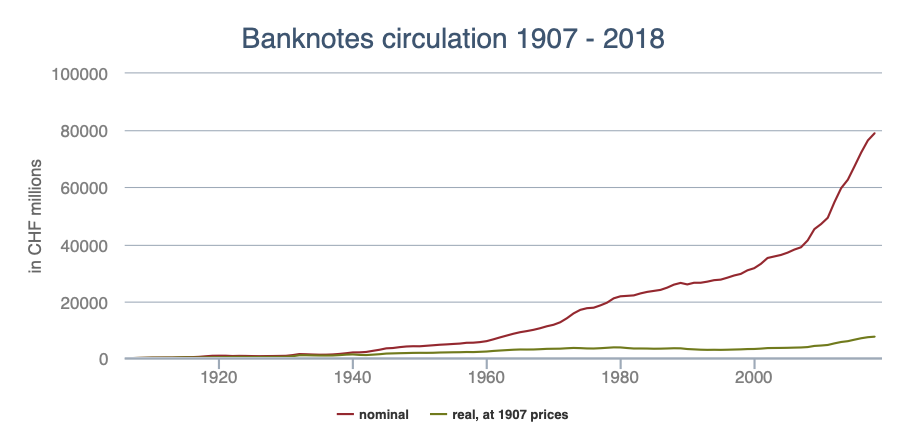

The most likely scenario predicts a decline in cash demand by 40-60% over the next 5-7 years. This represents a radical trend reversal in comparison to the past six years. Between 2012 and 2018, the value of banknotes in circulation grew from CHF 55 to 79 billion Swiss Francs or 44%.

Source: Swiss National Bank

Half of the respondents to a survey anticipate paying with cash just as often as they do now in the medium-term future

The scenario also contradicts a 2017 Survey on Payment Methods by the Swiss National Bank which concludes that 70% of payments were made in cash. Half of the respondents to the survey anticipate paying with cash just as often as they do now in the medium-term future.

Finally, the white paper did not foresee that card payments would face a systems outage on 19 November leaving customers unable to pay at major stores or purchase train tickets through the mobile app. A spokeswoman from SIX Payment Services confirmed the problem, “many customers could not pay with their card due to a technical problem, which affects all of Switzerland.” The outage was eventually resolved that same morning.

Download the full White Paper below:

This post is also available in:

![]()