The European Payments Council calls for further Dialogue between Stakeholders of the Cash Cycle

Chair, CashEssentials

This post is also available in:

![]()

According to a 2018 ECB survey, 75% of credit institutions rated their cashMoney in physical form such as banknotes and coins. More services to customers as important or very important, 20% were neutral, and only 5% rated cash services as unimportant. It is estimated that around 75% of all euroThe name of the European single currency adopted by the European Council at the meeting held in Madrid on 15-16 December 1995. See ECU. More banknotes withdrawn by customers are withdrawn via self-service banking, while deposits of banknotes are evenly split between attended (over-the-counter, OTC) services and unattended (automated) services.

Cost pressures are driving automation and reduction of ATM networks

The EPC report stresses that banks are pursuing the automation of cash services with a particular focus on deposit as traditional cash-out ATMs are increasingly replaced by cash-recirculating devices. However, the European ATM network is also downsizing, under the combined pressures of cost-cutting, banking consolidation but also increasing interoperability of different networks.

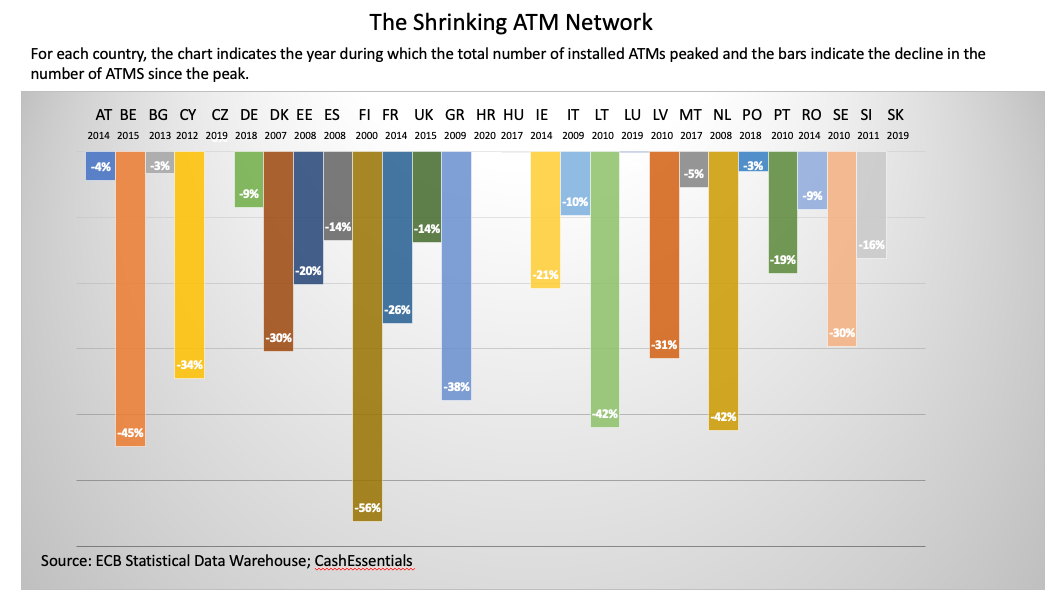

According to ECB data, 25,000 ATMs have been closed in the EU between 2014 and 2019. The chart below illustrates for each country, the year when the number of ATMs peaked and the decline in the number of ATMs since the peak year. Finland tops the league and saw its ATM estate shrink by 56% since 2000. Belgium has seen the fastest decline, with 45% of the ATMs closing since 2015.

Cash remains an important payment instrumentDevice, tool, procedure or system used to make a transaction or settle a debt. More for the time being and the foreseeable future

The recent ECB Study on the payment attitudes of consumers in the euro area (SPACE) shows that in 2019, cash remains by far the most widely used paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More instrument as 73% of the volume and 41% of the value Point-of-Sale (POSAbbreviation for “point of sale”. See Point-of-Sale terminal. More) and person-to-person payments was carried out using cash. down from respectively 79% and 54% in 2016. The EPC stresses that “consumers still use cash, and that they like to have choice in the way to pay”. It also emphasizes that a large segment of the population that does not have a choice at all. The European Commission, estimate that about 30 million adults in the EU do not have a bank account. Finally, cash plays and important contingency role and provides payment continuity when digital payment systems fail.

Less Cash Usage Increases the Cost of CashAlthough banknotes are delivered to the citizens free of charge and their use does not involve a specific fee, costs are generated during their manufacturing, storage and circulation process, which are covered by different social agents (central banks, commercial banks, retailers etc). More

The EPC concludes that the cash cycleRepresents the various stages of the lifecycle of cash, from issuance by the central bank, circulation in the economy, to destruction by the central bank. More is becoming increasingly complex and highlights a negative correlation between declining cash usage and increasing costs. As the use of cash for payments diminishes, then the unit costs tend to rise.

The EPC calls for a dialogue with all cash cycle stakeholders – including retailers and post offices – who could play a more important role in the distribution of cashActivity consisting of the delivery of cash throughout the territory in the amount and modality required to adequately cover the needs. It is one of the central bank’s core functions, for which the necessary logistics, materials and human resources are used, either in-house or outsourced. More. In particular, the EPC sees cashbackA service whereby the customer pays electronically a higher amount to a retailer than the value of the purchase for goods and/or services and receives the difference in cash. It is also a reward system associated with credit card usage, whereby the consumer receives a percentage of the amount spent on the credit card. More as an efficient alternative solution for the distribution of cash.

This post is also available in:

![]()