The Enduring Importance of Cash: Stabilisation of Cash in Circulation and Changing Withdrawal Patterns

The global payments industry often frames the future as a competition between cashMoney in physical form such as banknotes and coins. More and digital payments. Yet the latest data from the Bank for International Settlements (BIS) suggest a more nuanced reality. While consumers are increasingly using cards, mobile wallets and fast paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More systems for day-to-day transactions, cash continues to play a critical role for payments but also as a store of valueOne of the functions of money or more generally of any asset that can be saved and exchanged at a later time without loss of its purchasing power. See also Precautionary Holdings. More, a budgeting tool and a financial safety net.

The BIS paperSee Banknote paper. More “Tap a card, pay by phone, but cash still holds its own” draws on the 2024 Red Book statistics from the Committee on Payments and Market Infrastructures (CPMI). Its findings show that digital payments are growing rapidly across both advanced and emerging economies, but they also show that cash demand patterns are changing.

Stabilisation of Cash in Circulation Relative to GDP

The BIS brief highlights the stabilisation of cash in circulationThe value (or number of units) of the banknotes and coins in circulation within an economy. Cash in circulation is included in the M1 monetary aggregate and comprises only the banknotes and coins in circulation outside the Monetary Financial Institutions (MFI), as stated in the consolidated balance sheet of the MFIs, which means that the cash issued and held by the MFIs has been subtracted (“cash reserves”). Cash in circulation does not include the balance of the central bank’s own banknot... More as a percentage of GDP between 2016 and 2024 across many jurisdictions, underscoring the enduring role of cash in global economies. In 2024, cash in circulation averaged around 9% of GDP in advanced economies (AEs) and 6% in emerging market and developing economies (EMDEs),with notable outliers like Japan (21%) and Hong Kong SAR (19%) at the higher end, and Sweden (0.9%) and Türkiye (1%) at the lower end. This plateau suggests that cash is a critical store of value and a backup payment methodSee Payment instrument. More.

Decline in Cash Withdrawal Volumes

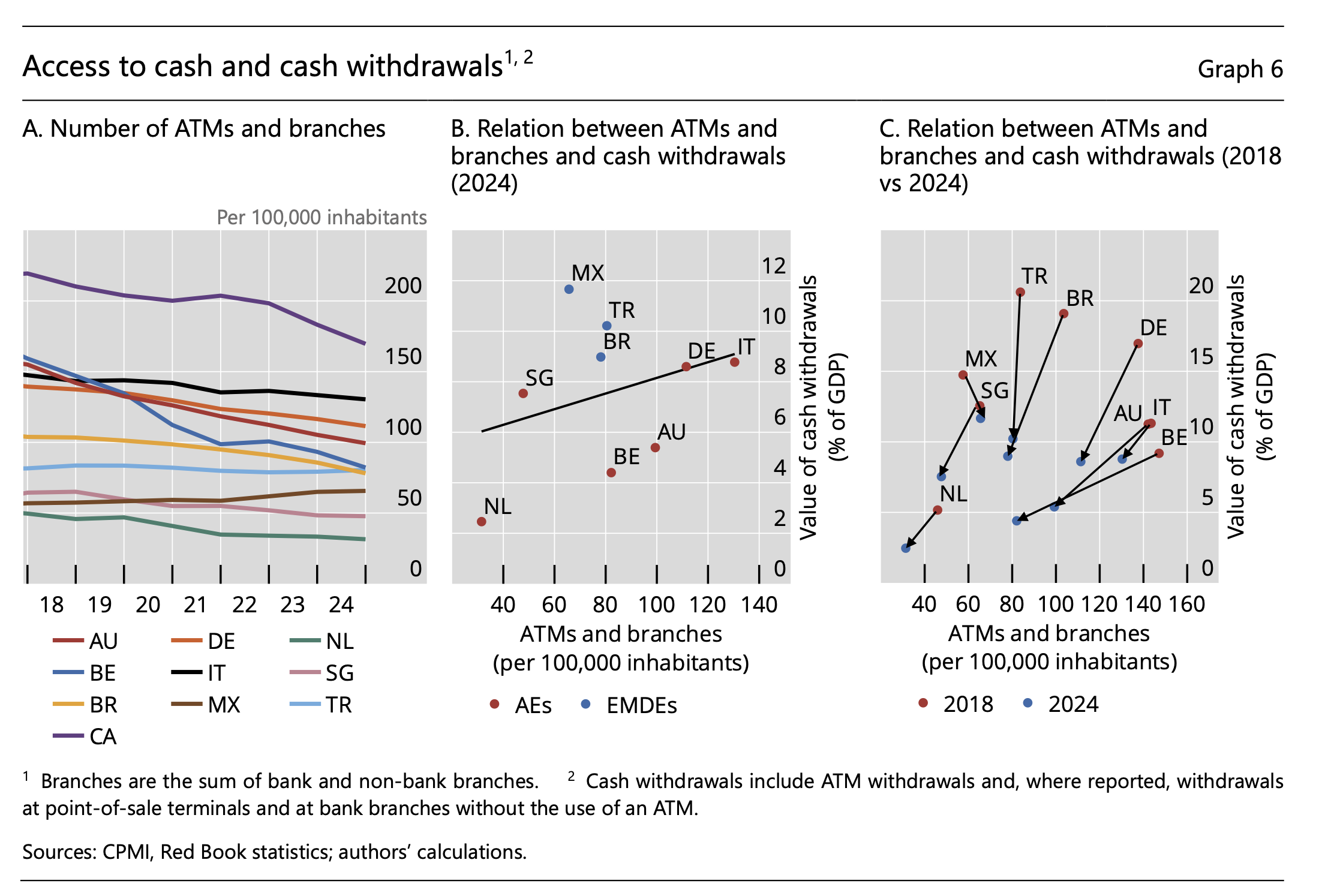

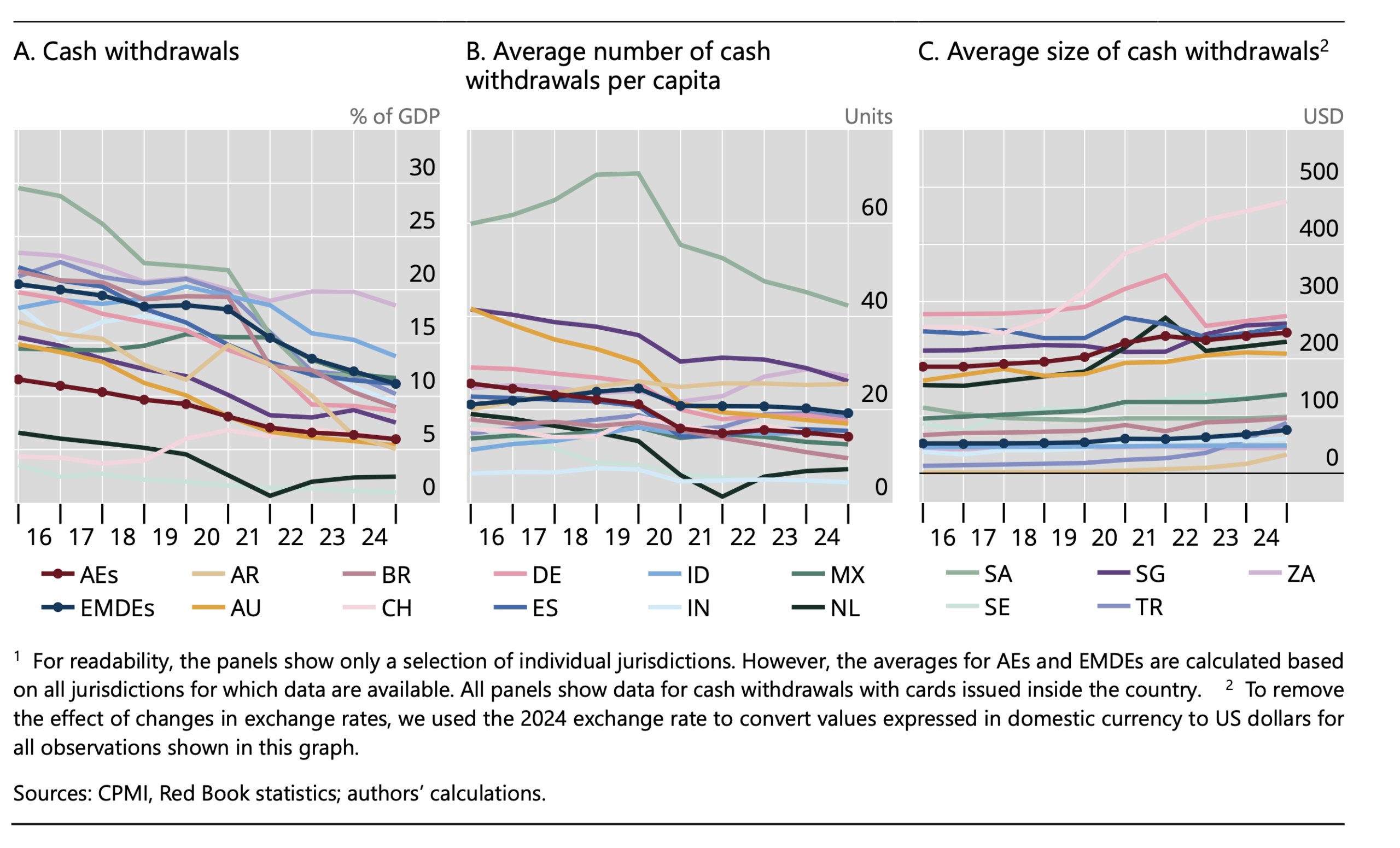

One of the most striking findings concerns the relationship between shrinking cash infrastructure and cash withdrawals. Across many countries, the number of ATMs and bank branches has fallen significantly in recent years (Graph 6 A). At the same time, the number of cash withdrawals per person has also declined (Graph 5 B). According to the BIS, jurisdictions with lower densities of ATMs and branches generally recorded lower cash withdrawal activity (Graph 6 C). In many cases, declining access points coincided with falling withdrawal volumes, even if the BIS cautiously refutes any proven causality, arguing that other factors may come into play including payments digitalisation.

Strategic Consumer Adaptation: Increasing Average Withdrawal Values

Despite the decline in cash withdrawal volumes, the average value of cash withdrawals has increased (Graph 5 C). This phenomenon suggests that while consumers are withdrawing cash less frequently, they are withdrawing larger amounts when they do. The increase in average withdrawal values can be interpreted as a strategic response by consumers to the reduced availability of cash access points. Facing longer travel distances and fewer ATMs, consumers may opt to withdraw larger sums to minimize the frequency of trips to cash access points, thereby reducing the inconvenience associated with declining infrastructure.

The increase in average withdrawal values is a significant trend, as it reflects consumers’ adaptation to the changing cash infrastructure landscape. This adaptation underscores the importance of maintaining a diverse and resilient cash access ecosystem to ensure universal access and financial inclusionA process by which individuals and businesses can access appropriate, affordable, and timely financial products and services. These include banking, loan, equity, and insurance products. While it is recognised that not all individuals need or want financial services, the goal of financial inclusion is to remove all barriers, both supply side and demand side. Supply side barriers stem from financial institutions themselves. They often indicate poor financial infrastructure, and include lack of ne... More.

Implications for Monetary Policy and the Future of Cash

The trends in cash infrastructure and withdrawal patterns have significant implications for monetary policy and financial inclusion. The decline in cash infrastructure can lead to financial exclusion, particularly for vulnerable populations such as the elderly, low-income households, and rural communities who rely heavily on cash transactions. Ensuring universal access to cash is crucial for maintaining financial inclusion and the resilience of the financial system.

This is why the future of cash should not be framed solely in terms of transaction shares. Even if digital payments continue to grow, the public value of cash extends beyond its share of retail purchases. Physical currencyThe money used in a particular country at a particular time, like dollar, yen, euro, etc., consisting of banknotes and coins, that does not require endorsement as a medium of exchange. More provides universal acceptance, privacy, financial inclusion and operational resilience in ways that purely digital systems cannot fully replicate. Or as the BIS puts it « … is impossible to imagine a world without cash, as it still plays a prominent role in people’s lives. »