The Use of Cash in the Euro Area during the Covid-19 Pandemic

Ph.D. in U.S. History, Columbia University in the City of New York

Post-Doctoral Researcher in Global Correspondent Banking, 1870-2000 – Mexico and South America, University of Oxford

This post is also available in:

![]()

In a July 2021 paper for the European Central Bank (ECB), Barbora Tamele, Alejandro Zamora-Perez et al. assessed cashMoney in physical form such as banknotes and coins. More circulation in the euroThe name of the European single currency adopted by the European Council at the meeting held in Madrid on 15-16 December 1995. See ECU. More area during the Covid-19 pandemic. The authors also examined the role of cash as a possible transmission vector of the SARS-CoV-2 virus.

This post summarizes the findings in the first part of the paperSee Banknote paper. More relating to the increase in the circulation of cash in the euro area during the Covid-19 pandemic, associated with the so-called cash paradox: the European public is holding more cash for precautionary purposes, even though Europeans use less cash to realize transactions. The post also examines the data from the ECB IMPACT survey (July 2020) on the impact of the Covid-19 pandemic on cash usage in the Euro area.

During the Covid-19 Pandemic, the Increase in the Precautionary Demand for Cash More than Made Up for the Decrease in Cash Usage in Payments

“Cash is seen as a safeSecure container for storing money and valuables, with high resistance to breaking and entering. More haven in all crisis situations, including the Covid-19 pandemic. In times of insecurity, people tend to increase their precautionary holdingsBanknote demand motivated by the store of value function of banknotes, for saving purposes or as a precaution for uncertainties. See Hoarding. More of cash to be prepared for whatever lies ahead. […] The increase in the overall demand for cash during the Covid-19 pandemic was extraordinary compared with pre-crisis years, mainly due to higher store-of-value demand from euro area citizens.” – Tamele, Zamora-Pérez et al. 2021: 26.

Tamele et al. found that although the pandemic caused a decline in the demand for cash as a payment instrumentDevice, tool, procedure or system used to make a transaction or settle a debt. More, it also caused a more considerable increase in the store-of-value demand (or precautional demand) of cash, as the public held on to cash as the pandemic translated into a crisis-like situation.

The phenomenon is not specific to the euro area. Antti Heinonen has demonstrated that most countries around the world experienced a run for cash in 2020 due to the Covid-19 pandemic.

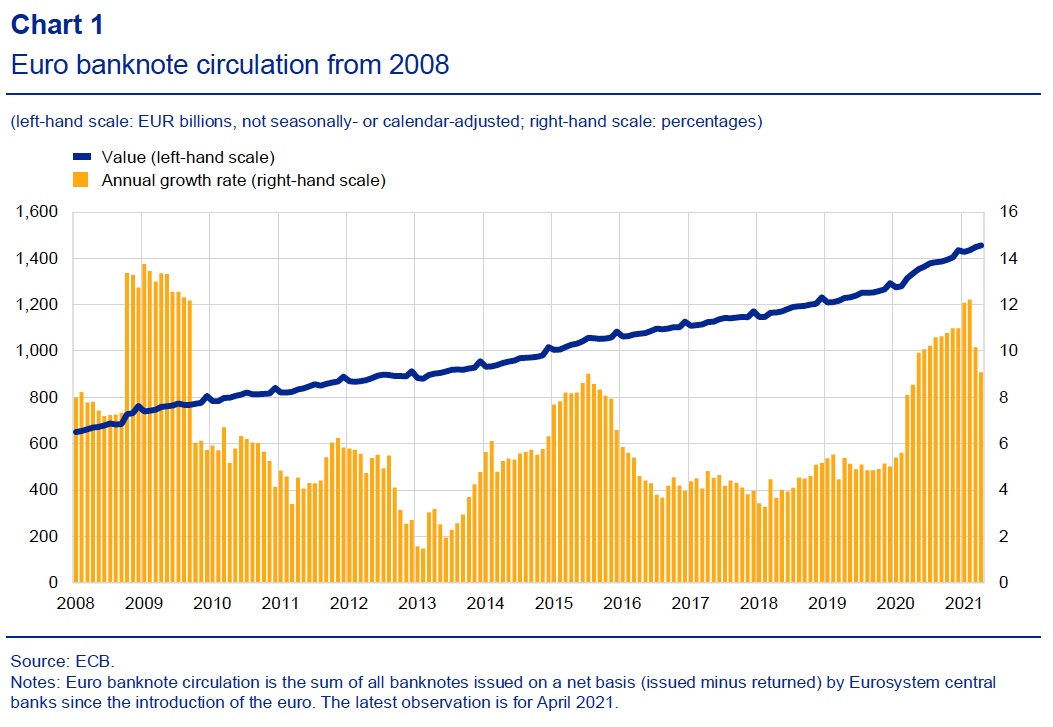

Graph 1. Euro BanknoteA banknote (or ‘bill’ as it is often referred to in the US) is a type of negotiable promissory note, issued by a bank or other licensed authority, payable to the bearer on demand. More in Circulation, January 2008-April 2021

Source: Tamele, Zamora-Pérez et al. 2021: 5.

The circulation of euro banknotes grew by 12% in February 2021 compared with February 2020, the last month before the Covid-19 pandemic spread throughout the euro area (see Graph 1). The annual growth rate slowed in March (10%) and April (9%). Still, these figures are significantly higher than the roughly 5% average annual growth observed in equivalent periods in the five years before the Covid-19 pandemic (2015-2020).

Banknote Flows

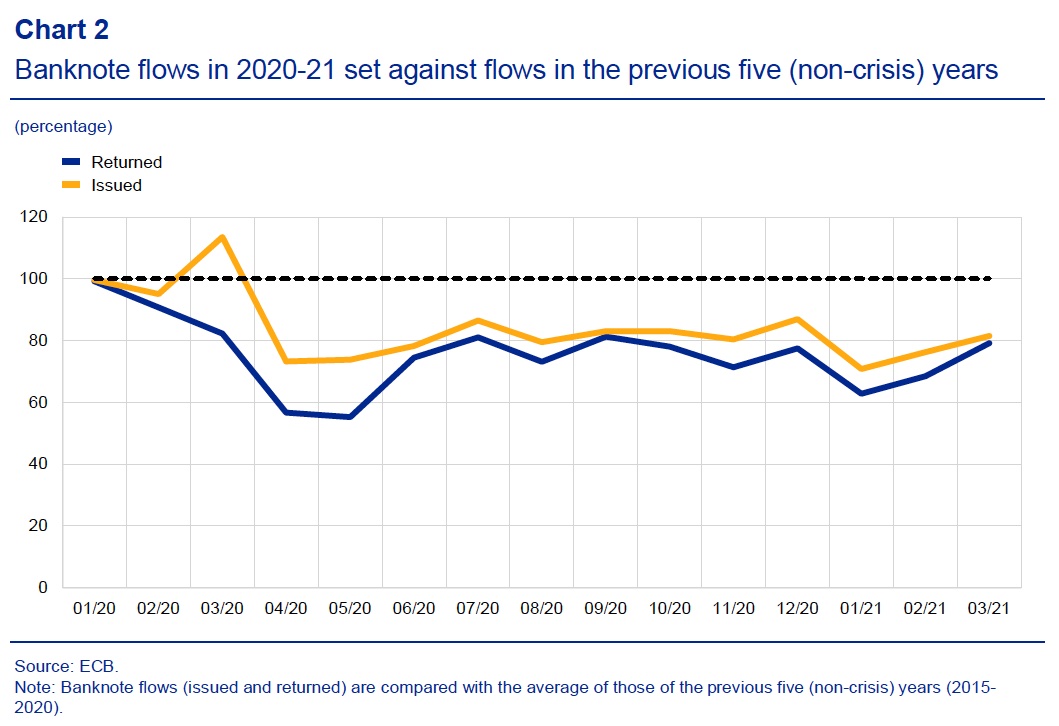

In prior crises, banknote circulation increased due to higher banknote withdrawals leading to higher gross issuanceValue of banknotes issued by a central bank over a period. More by central banks. During the onset of the Covid-19 pandemic, the value of banknotes issued by central banks fluctuated at around 70-90% of the average level of the previous five years, yet the value of banknotes returned to central banks decreased even further, at approximately 60-80% of normal levels (see Chart 2).

Graph 2. Euro Banknote Flows, 2015-2020 and 2020-2021

Source: Tamele, Zamora-Pérez et al. 2021: 6.

The increase in circulation of small denominationEach individual value in a series of banknotes or coins. More banknotes (€5, €10, €20) was lower than the increase in higher denomination banknotes, as the public favors the latter pieces as reserves to store value.

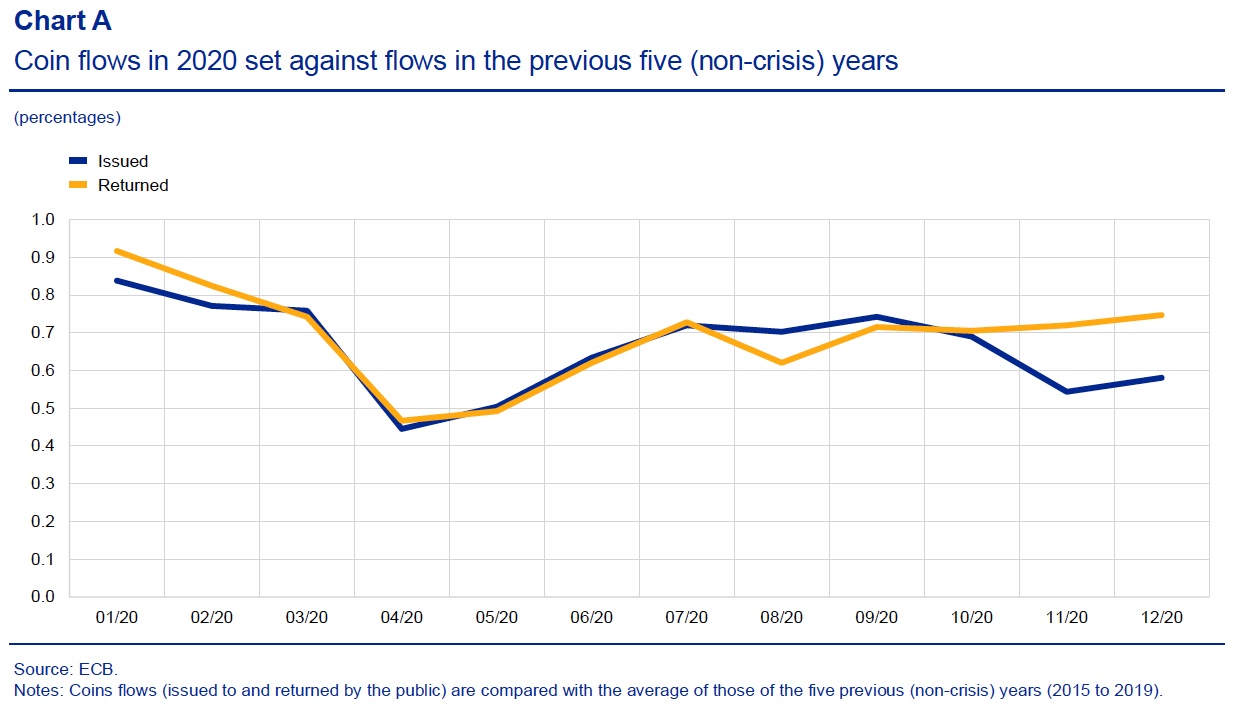

CoinA coin is a small, flat, round piece of metal alloy (or combination of metals) used primarily as legal tender. Issued by government, they are standardised in weight and composition and are produced at ‘mints’. More Flows

In February 2021, euro coins in circulation grew by only 1.6% year on year (see Graph 3), a far slower growth rate than banknotes (12%). Although both banknotes and coins are used for transactions, coins are rarely used to store value.

Graph 3. Euro Coin Flows, 2015-2020 and 2020-2021

Source: Tamele, Zamora-Pérez et al. 2021: 7.

Fears over the Role of Cash in the Transmission of Covid-19 and Government Measures Impacted Cash Usage

Nearly half (49%) of the respondents to the ECB-commissioned IMPACT survey (2020) reported employing cash “the same as before” the Covid-19 pandemic, and 10% said they used cash more often. Only 39% said they were using cash less often (see Graph 4).

Graph 4. Cash Usage in Europe as per the IMPACT Survey, July 2020

Source: Tamele, Zamora-Pérez et al. 2021: 8.

A plurality of 45% of respondents paying in cash less frequently said they found electronic payments more convenient. About 38% of respondents mentioned they were afraid of using cash as a potential transmission vector of Covid-19. 33% of those surveyed thought they would be at risk of getting the SARS-CoV-2 virus via hand contact or proximity to the cashierInitially, the person who is responsible for the safe, its opening and closing, and the contents that are safeguarded inside it. Nowadays, at a central bank, the person who is responsible for matters related to the treasury and cash. Their signature would usually appear alongside others on the banknotes issued by the bank. More (see Graph 5). A share of 35% cited government recommendations to avoid cash.

Graph 5. Reasons for Using Cash Less Often, July 2020

Source: Tamele, Zamora-Pérez et al. 2021: 9.

Respondents with higher education levels were more concerned about infection through banknotes (42%) than those with secondary (36%) or primary (33%) education; urban respondents were more worried (40%) than rural respondents (35%). When looking at the overall population in the survey, 30% of respondents asserted being fairly concerned about the risk of contracting the SARS-CoV-2 virus from banknotes, and 11% were very concerned (see Graph 6). The majority of respondents (55%) said they were either not very concerned (37%) or not concerned at all (18%) about contracting Covid-19 from cash.

Graph 6. Concerns about Cash as Transmission Vector of SARS-CoV-2, July 2020

Source: Tamele, Zamora-Pérez et al. 2021: 9.

This post is also available in:

![]()