A Newcomer to the U.K.: Cash and Digital Payments

Ph.D. in U.S. History, Columbia University in the City of New York

Post-Doctoral Researcher in Global Correspondent Banking, 1870-2000 – Mexico and South America, University of Oxford

This post is also available in:

![]()

In March, as I prepared to travel to Oxford (my second international move since returning to Mexico City from New York City in December 2020), my parents insisted I carry a fraction of my savings in cashMoney in physical form such as banknotes and coins. More and took me to Mexico City’s airport to buy sterlingPound sterling, British currency. More pounds. Most foreign exchangeThe Eurosystem comprises the European Central Bank and the national central banks of those countries that have adopted the euro. More dealers listed the pound as a currencyThe money used in a particular country at a particular time, like dollar, yen, euro, etc., consisting of banknotes and coins, that does not require endorsement as a medium of exchange. More there, but only one had the amount I demanded in banknotes. There are only two daily flights to London, a small amount compared to flights from Mexico City to U.S. destinations.

My parents’ concern was correct and prescient. As a newcomer, I have faced many frictions while conducting transactions due to the dominance of digital payments in the United Kingdom. The cash I purchased in Mexico City and Revolut and Wise multicurrency accounts mitigated a long and unsuspected period of financial exclusion. It took me over two months to open a U.K. bank account, which I will discuss in another blog entry.

Heathrow Terminal C Arrivals

I arrived for the first time in England on March 22. When I took The Airline’s bus from Heathrow to Oxford, the driver said I could pay using a card in my iPhone’s mobile wallet. I spent with my U.S. Apple Card and assumed the transaction had cleared immediately. However, this was not the case. Goldman Sachs Bank (Apple’s credit card partner) immediately flagged and rejected the transaction.

Two days later, I hopped on a bus operated by the same company. Shortly after, I received a notification for a USD45 charge. Thinking it was an error, I emailed the bus operator and disputed the charge with Apple Card. An employee from the Oxford Bus Company told me:

“These are funds that have been recovered from an initially declined transaction on the 21/03/2023, once you have used the same payment methodSee Payment instrument. More on our services again, the charge has been applied.”

That is, the fare from the airport cleared until I used another bus again. While paying for the bus in Heathrow might have been fast, it took me several days, iMessage, and emails to ascertain whether the transaction was legitimate. So much for convenience.

Buses in Oxford take cash and contactless payments, but they only advertise the latter conspicuously. I thought I could not use cash to pay for my trips until I saw a senior woman giving cash to a bus driver.

Retailers

I sought to pay using cash whenever possible, as most international credit cards carry heavy transaction fees and give inconvenient exchange rates. However, many coffee shops and restaurants in Oxford have gone cashless. Retailers often advertise they are cashless establishments in their frontFacade, face. See Obverse. More doors and registries. Some pubs have dedicated terminals for tipping with cards and contactless payments.

The profusion of electronic point-of-sale (POSAbbreviation for “point of sale”. See Point-of-Sale terminal. More) terminals is notable even among street vendors. Most stalls at the food market in Gloucester Square (next to my office) take contactless payments. These vendors are willing to pay high interchange fees and commissions due to customers’ shift towards digital payments since the Covid-19 pandemic. On the consumers’ side, credit card debt has increased, a problem worsening with the Bank of England’s interest rate hikes to curb inflation.

Access to Cash in the United Kingdom

In Oxford, as in other rural England towns, there are a few bank branches and ATMs. Most are in the city centre. U.K. bank branches declined 28% between 2012 and 2020; ATMs dropped 29% between 2015 and 2020. The decline in cash infrastructure is somewhat alleviated as customers can withdraw cash at no cost from all bank ATMs even if they do not have an account. Some supermarket companies have banks, such as Sainsbury’s.

In May 2021, Barclays, HSBC, Lloyds, Nationwide, NatWest, Santander, and other banks committed to protecting access to cash through UK Finance, an industry group. They also established the Access to Cash Action Group (CAG).

CAG supported the launch of bank hub pilots for customers living in areas with scarce cash and banking services. Banks agreed for LINK to assess and develop recommendations to improve communities’ access to cash in December 2022.

On December 19, 2022, nine commercial banks launched Cash Access UK, a non-profit helping to protect cash access. On the launch, David Postings, chief executive of U.K. Finance, said,

“While many people are now opting to manage their moneyFrom the Latin word moneta, nickname that was given by Romans to the goddess Juno because there was a minting workshop next to her temple. Money is any item that is generally accepted as payment for goods and services and repayment of debts, such as taxes, in a particular region, country or socio-economic context. Its onset dates back to the origins of humanity and its physical representation has taken on very varied forms until the appearance of metal coins. The banknote, a typical representati... More digitally, we want to ensure that people can continue to access cash and do their banking face to face too.”

Cash and Immigrant Communities

Getting used to paying with your phone is straightforward until it isn’t. I assumed the Turkish barber would take card payments the second time I got a haircut. When he finished and requested paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More of ₤21 in cash, I asked him where the nearest ATM was, gave him a ₤10 note and a ₤1 coinA coin is a small, flat, round piece of metal alloy (or combination of metals) used primarily as legal tender. Issued by government, they are standardised in weight and composition and are produced at ‘mints’. More, and told him I would be right back with the rest. Fortunately, a white-label ATM at a Cooperative nearby allowed me to pay for my haircut without further delay.

U.K. inflation is galloping due to Brexit, the pandemic supply shock, the war in Ukraine and high energy prices. Immigrant communities and working-class families are in dire straits to make ends meet during this cost-of-living crisis. Many people are using cash to budget, as the #cashstuffing trend attests.

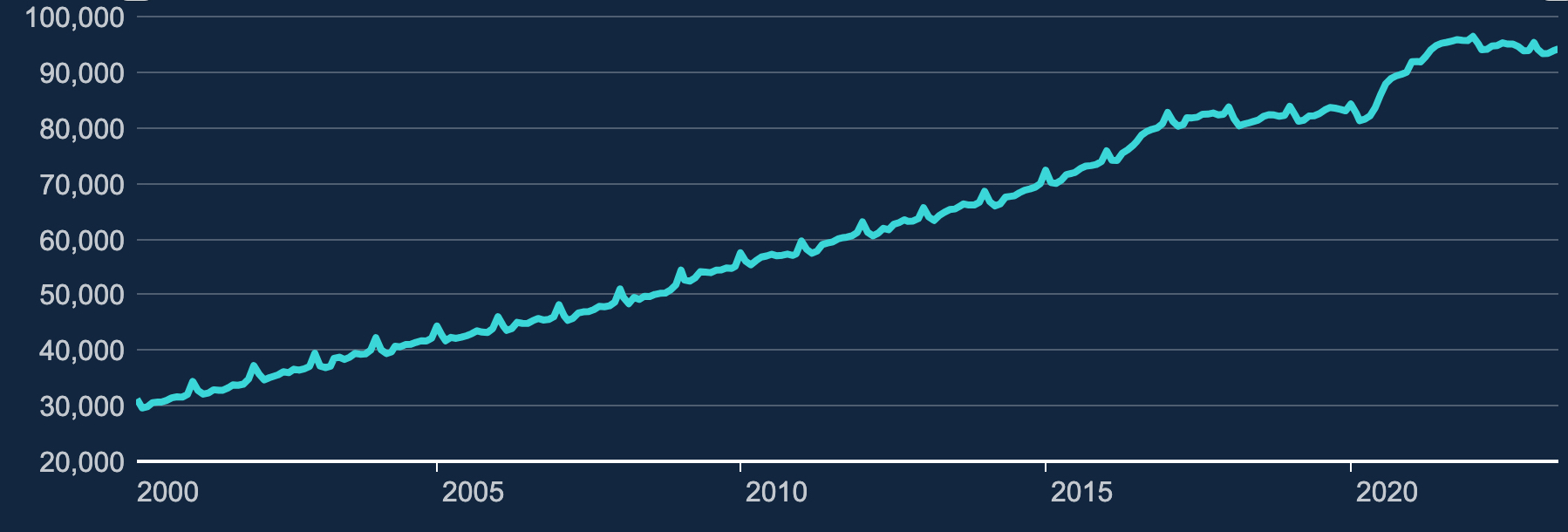

Graph 1. United Kingdom: Notes and Coins in Circulation, January 2000-May 2023 (millions of British sterling pounds).

Note: Variable excludes backing assets for commercial banknoteA banknote (or ‘bill’ as it is often referred to in the US) is a type of negotiable promissory note, issued by a bank or other licensed authority, payable to the bearer on demand. More issues in Scotland and Northern Ireland from October 2009.

Source: LPMAVAA, Bank of England (2023).

At Lidl the other day, I saw that an immigrant worker had to leave a pieceIn plural, it is commonly used as synonym for units of banknotes and coins. More of bread behind at the registry. He paid for his other items (some cherry tomatoes and spaghetti) with cash. Having already paid for my groceries with my phone, I did not have the cash to help him with the check. That day, digital payments prevented me from aiding someone when I could. I made a mental note never to forget to carry some loose changeThis is the action by which certain banknotes and/or coins are exchanged for the same amount in banknotes/coins of a different face value, or unit value. See Exchange. More.

This post is also available in:

![]()