Impacts of Recent Developments on the Cash Cycle: A Global Analysis

Even though innovations in digital payments have accelerated in recent decades, cashMoney in physical form such as banknotes and coins. More is the only paymentA transfer of funds which discharges an obligation on the part of a payer vis-à-vis a payee. More option for a number of citizens in every country. Moreover, the great majority of people would like to keep cash as one of their payment options even in those countries where its share in transactions is already small. Cash is also used for precautionary reasons as well as a store of valueOne of the functions of money or more generally of any asset that can be saved and exchanged at a later time without loss of its purchasing power. See also Precautionary Holdings. More and has a significant role in various crises and uncertainties.

In order to continue to be a safeSecure container for storing money and valuables, with high resistance to breaking and entering. More haven in the future, cash infrastructure should be maintained and developed in line with the changing environment. Only a structure that functions in normal circumstances can be used in a crisis. Therefore, with good reasons, there is a debate in several countries about the status of the cash infrastructure.

Recent discussions have mainly focused on the access to and acceptance and affordability of cash, and new useful indicators have been created to measure these.

However, these indicators only partly describe the impacts of current developments. Nor can the impacts be analysed by the development of the value of cash in circulationThe value (or number of units) of the banknotes and coins in circulation within an economy. Cash in circulation is included in the M1 monetary aggregate and comprises only the banknotes and coins in circulation outside the Monetary Financial Institutions (MFI), as stated in the consolidated balance sheet of the MFIs, which means that the cash issued and held by the MFIs has been subtracted (“cash reserves”). Cash in circulation does not include the balance of the central bank’s own banknot... More or its ratio to GDP. These might have been valid indicators when the value of cash correlated strongly with the share of cash in transactions. Furthermore, the value of cash or its ratio to GDP at a certain point in time is a stock variable, while the different components of the cash cycleRepresents the various stages of the lifecycle of cash, from issuance by the central bank, circulation in the economy, to destruction by the central bank. More – like production, processing or transport of cash – are flow variables. All these activities are moreover volume businesses; hence focusing just on values is insufficient or even misleading.

The impacts of decreasing volumes on the cash cycle are already seen in a few countries. In order not to have a vicious circle, developments should be consistently followed and proactively responded to by the respective authorities.

The following study is a preliminary attempt to find better metrics to indicate what is happening in cash cycles globally. It will also indicate how central banks have succeeded in making the cash cycle more efficient. In principle, the whole cash cycle should be analysed in this context from production, distribution and processing up to destruction. The publicly available information limits the following study to the banknoteA banknote (or ‘bill’ as it is often referred to in the US) is a type of negotiable promissory note, issued by a bank or other licensed authority, payable to the bearer on demand. More data provided by central banks, but at the national level all stakeholders in the cash cycle should be included in the exercise.

An example to clarify the issue at stake

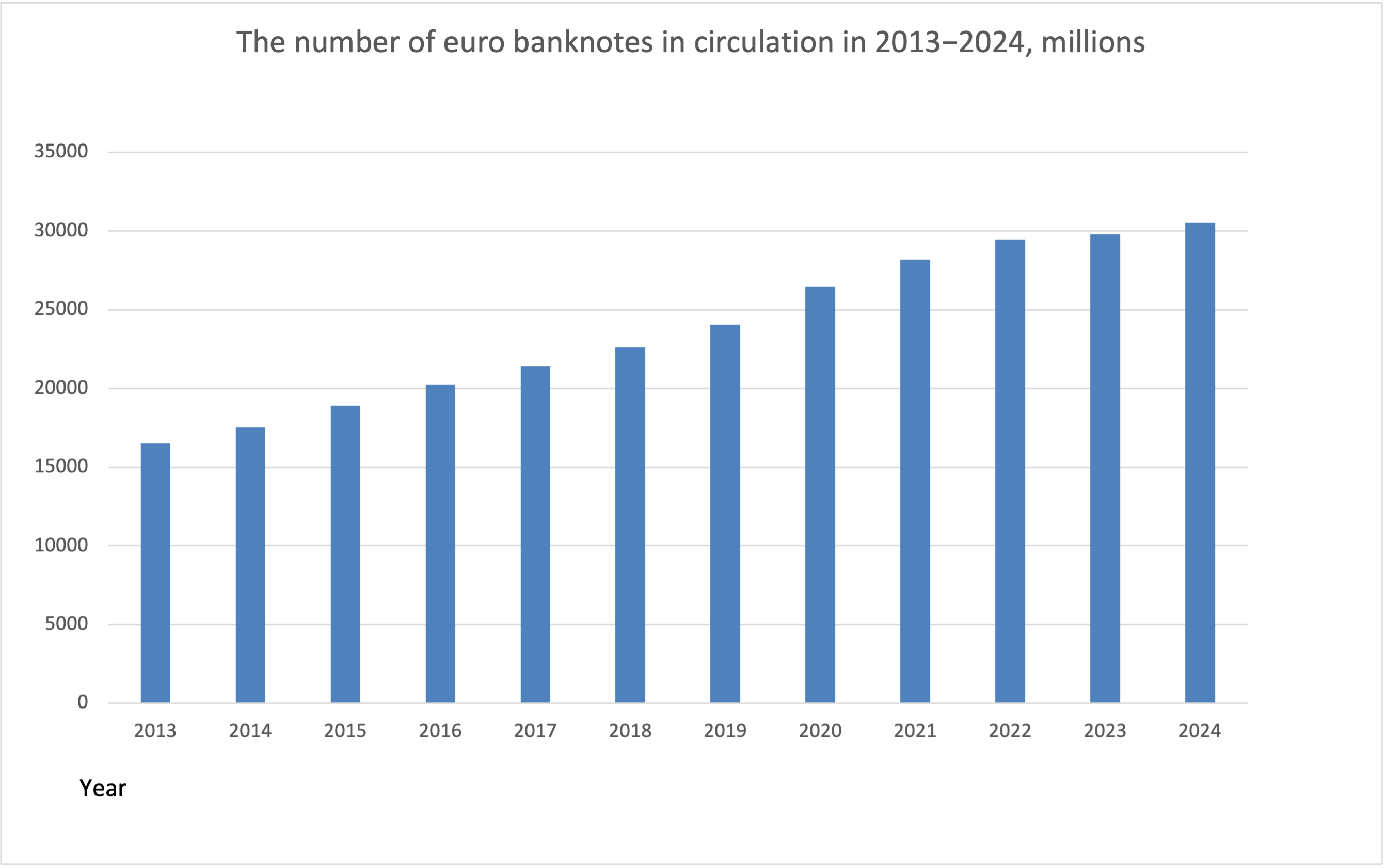

To clarify the issue at stake and before moving to address the situation globally, developments of euroThe name of the European single currency adopted by the European Council at the meeting held in Madrid on 15-16 December 1995. See ECU. More banknotes, one of the few cases of full transparency of volume figures as well as both stock and flow variables, is used as an example. Figure 1 represents the number of euro banknotes at the end of each year from 2013 to 2024.

Fig 1: The number of euro banknotes in circulation in 2013−2024 (millions of pieces). Source: ECB Data Portal.

According to this chart, the impression of the recent development of euro banknote circulation is very encouraging: the number of euro banknotes in circulation has grown every year during the last decade. Also, the significant increase during Covid-19 pandemic is evident.

However, the annual stock figures give only a partial picture. The next step is to check what kind of flows have led to this stock development. This is done by looking at the annual lodgements and withdrawals of euro banknotes, as described in Figure 2.

Fig 2: The number of euro banknotes lodged and withdrawn in 2013−2024 (millions of pieces) Source: ECB Data Portal

This figure, describing the development of banknote flows to and from the EurosystemThe Eurosystem comprises the European Central Bank and the national central banks of those countries that have adopted the euro. More central banks, gives a totally different picture. Both flows have decreased almost continuously and around 30% during the period. In particular, the drop during the pandemic in 2020 was significant, and since then the flows have recovered only slightly. This development means that the transport of euro banknotes to and from the Eurosystem central banks and their processing have also decreased correspondingly. Similar conclusions could be drawn from the development of US dollarMonetary unit of the United States of America, and a number of other countries e.g. Australia, Canada and New Zealand. More note circulation.

One may ask, what is the problem, because that is just what the central banks have pursued? By increasing local recirculationThe right to recirculate banknotes that have been checked for authenticity and sorted for fitness by banks and cash-in-transit companies. The right is normally based on rigorous rules established by the central bank. More, the cash cycle has become more efficient. Furthermore, these developments are good news from the point of view of the environmental impact of banknotes.

However, the problem is that the decreasing flows may create challenges in the medium term from the perspective of the cash infrastructure and various stakeholders in the cash cycle. In the following recent developments are studied globally.

Global developments of banknote stocks

Let us first study the global development of banknote circulation in volume terms. Currently, there are close to 150 different currencies issued by central banks and other monetary authorities. The number is significantly lower than that of the independent states, because several currencies are issued by monetary unions and/or they are used outside the state or monetary area responsible for their issuance.

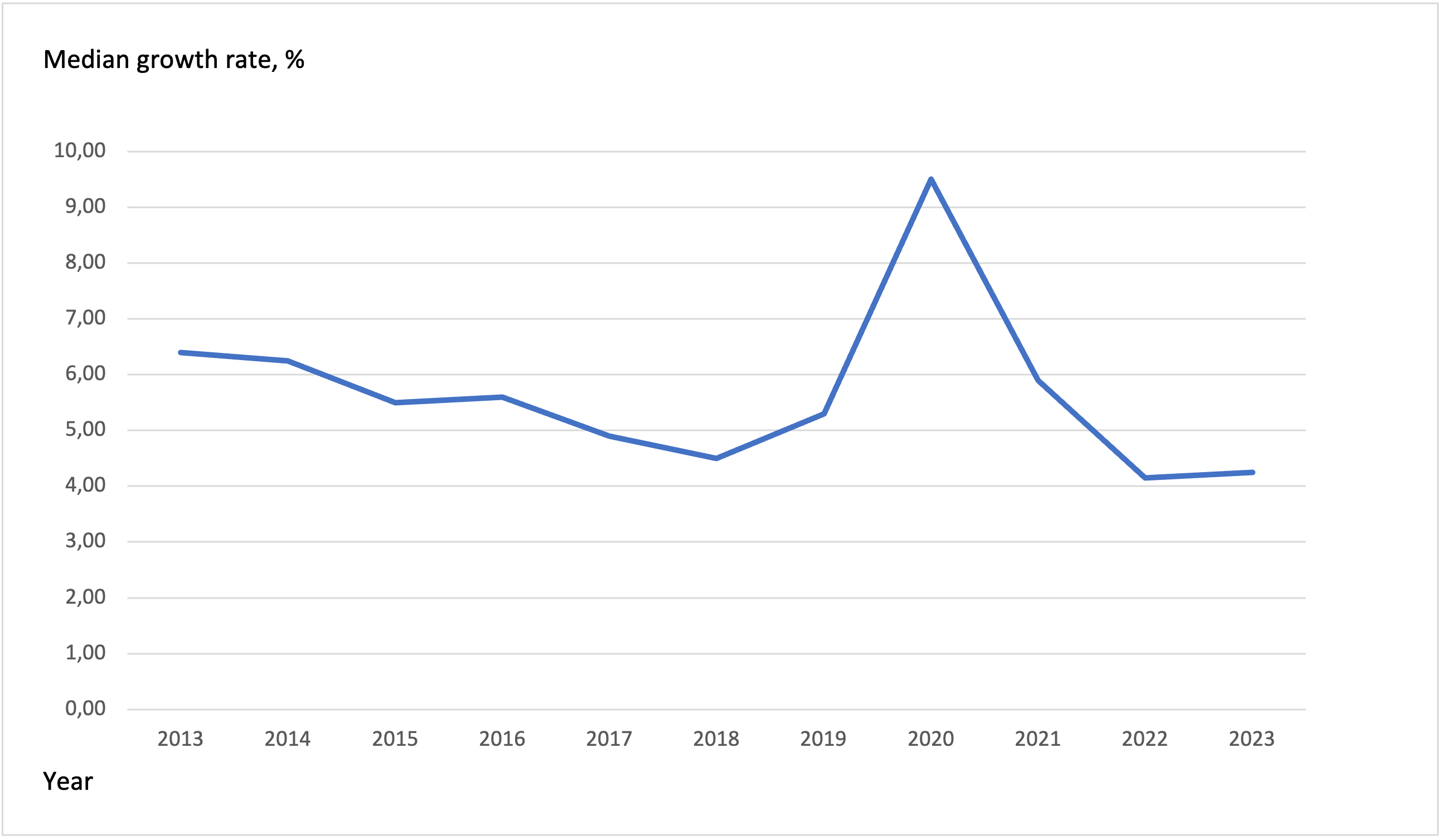

Data on cash in circulation in value terms are regularly available for around 140 currencies. Regular data on the more important variable of the number of banknotes in circulation is limited, however, to a good 100 currencies. Figure 3 describes how the median growth rate of the number of notes in circulation has evolved globally at the end of the years 2013−2023.

Fig 3: Median growth rate by the number of banknotes in circulation in 2013−2023, on average 108 currencies [1]

Based on Figure 3, the median growth rate by the number of banknotes in circulation has exceeded 4% during the whole period. This means that at least half of the c. 108 currencies have had a growth rate higher than 4%. The second observation is the exceptional development during the Covid-19 pandemic, when the median growth rate was more than 9%.

Another way to study the global development is to count the share of currencies which have had a positive growth rate by the number of banknotes in circulation at the end of various years. This development during the last decade is depicted in Figure 4.

Fig 4: Per centFraction of a currency representing the hundredth of the unit of account. More of currencies which had a positive growth rate by the number of banknotes in circulation in 2013−2023, on average 108 currencies

The pandemic and its aftermath of growing inflation was a global phenomenon, but otherwise the different annual developments are explained mainly by local situations. A negative growth rate doesn’t necessarily mean that people have changed their behaviour towards the use of banknotes. When a new higher denominationEach individual value in a series of banknotes or coins. More is introduced, the store of value denomination often changes. This evidently decreases the number of banknotes in circulation, when for example five pieces are replaced by just one. Similarly, when the lowest denomination is withdrawn from circulation, the number of banknotes may decrease temporarily.

On the basis of Figure 4, more than 80% of the currencies have had annually a positive growth rate during the last decade except in years 2022 and 2023, when it was a bitIn computers, the basic unit of digital information; contraction of BInary digiT. More lower. A decline in this share was foreseen after the exceptional increases of the note stocks in 2020. They have subsequently been given up gradually in an environment of growing inflation and interest rates.

However, as shown by the earlier example on euro banknotes, various flow developments may have led to the growth rates of the annual note stocks. These flow developments will be considered next, and particularly what kind of conclusions can be drawn on their impact on the cash cycle.

Global development of banknote flows

As a balance sheetA piece of paper or substrate of 800 mm by 700 mm, on which banknotes are printed. The “sheet to sheet” printing technique is the most widely used in printing of banknotes, but the roller printing technique also exists. More item, cash in circulation is similar to other liabilities of a central bank and hence it is appropriate to address it in value terms. Nevertheless, when considering cash related activities, they are all volume driven. This difference is unfortunately not taken consistently into account by central banks in annual reports and other data published on their websites because value data are often used when describing cash related developments. In many cases lodgements and withdrawals of notes are addressed in value terms, not to mention their production, processing or destruction.

More than 70 central banks provide regularly at least some information on activities related to banknote flows. Based on these data a global view of the impacts of recent developments has been studied.

Starting from note production, only some 25 central banks provide regular annual information on it. It is a too small figure to draw any global conclusions. Furthermore, the annual production needs of central banks vary significantly from year to year. They are high before the introduction of a new series or upgrade, because central banks are conservative in their estimates of the needs. After the issuance of a new series the needs often drop significantly and start to increase again only gradually.

The next step in the cash cycle is the issuance and return of notes and their processing. Figures of the withdrawals and lodgements and/or their processing are provided by 65 issuing authorities. However, 18 central banks provide only or mainly value figures, which do not necessarily tell anything about the volume flows. More than 42% of those central banks, which provide data on volume flows, have decreasing and 22% increasing flows. The developments of the rest have no clear trend.

The final step in the note cash cycle is their destruction. Destruction of notes is a very important component because it explains the replacement demand for unfit banknotes. The banknote order of central banks consists of three components: new demand, replacement demand and inventory adjustments. As explained in Figure 3, the annual median growth rate was between 4% and 6.5% during last decade except in 2020 and major adjustments in inventories occur only irregularly. Hence, the replacement demand for unfit notes is often the main explanation of the size of the banknote order, except in the case of introduction of a new series or upgrade.

50 central banks provide regular information on the destruction of notes. The industry has made great efforts to increase the durability of banknotes, so it is not a surprise that the destruction of notes has rarely an increasing trend. Furthermore, the decreasing transactional use of notes reduces wear and tear of notes and increases their lifetime.

Only 13 % of those currencies, from which volume data is available, have an increasing trend. Others have either a decreasing or no clear trend is evident.

Metrics of banknote volume flows

In order to have a metric, lodgement/processing and destruction flows should be set in proportion to something. Two indicators have been considered in this respect: return frequency and destruction rateRatio between the number of banknotes destroyed over a given period of time and the number of banknotes processed (cleared) during that same period. Expressed as a percentage, it indicates the number of banknotes destroyed for each hundred banknotes processed. The destruction rate depends on many factors, including but not limited to the quality policy followed by the central bank. There tends to be notable differences in the destruction rates between denominations, the rates generally being muc... More. The return frequency is the ratio between lodgements/processing and notes in circulation and the destruction rate the ratio between destroyed notes and notes in circulation. [2]

The return frequency can be counted for 56 and the destruction coefficient for 48 currencies. One or the other is available from 74 currencies covering all continents, which gives a reasonable description of the global situation. The data is not covering the full decade 2013 (2014)−2023 (2024) in all cases and an average of the two first years and two last years of the period are used in the study to minimise the impact of potential exceptional circumstances.

The development of return frequency and destruction rates during the period are divided in five categories: significant decrease (more than 50%), moderate decrease (20%−50%), stable (20 > decrease > -20%), moderate increase (20−50%) and significant increase (more than 50%). The results are depicted in Figure 5.

Fig 5: The development of return frequency and destruction rate of banknotes during the last decade.

As regards both indicators, the metrics have a moderate or significant decrease in a great majority of currencies; 71% of the currencies belong to these two categories. The rest has mostly a stable situation and only very few currencies have an increasing trend. The results could have been even more striking if the time period had been longer because in the case of many currencies the durability improvements were already made before 2013.

A typical development of many currencies has been a decreasing trend up to 2020, when – because of lockdowns and travel restrictions – both lodgements and processing decreased significantly. Therefore, in many cases both metrics increased in 2021 and have either stabilised or continued to decrease thereafter.

Concluding observations

The objective of this study has been to consider the impact of recent developments on the cash cycle and to find representative indicators for global developments. Cash related analyses are often based on the value of cash in circulation or on its ratio to GDP. Even if these considerations have their role, they tell very little about the main components of the cash cycle: the production, issuance, processing or destruction of banknotesA process by which a central bank destroys banknotes that are unfit to return into the fiduciary circulation. This is the last step in the life of the banknote. The destruction can be done manually or mechanically, and the latter may be online or offline. Online destruction is directly performed by automated sorting machines, without interruption of the treatment process. The process needs to be controlled in a very special way, since there is no possibility of verification or reconciliation. More. Therefore, it is important to develop representative metrics for the volume developments of cash related activities.

Figure 5 represents a preliminary attempt to find a metric for two components of the cash cycle: the return frequency and destruction of banknotes. The result does not surprise and is very much in line with the objectives of central banks.

Recent efforts have focused on the efficiency of the cash cycle and on the increase of the note lifetime by introducing more durable substrates. However, the impacts may require innovative solutions to keep the cash cycle viable to all stakeholders.

[1] In order to have as extensive data as possible the number of currencies included varies a bit, because data are not available from all currencies during the whole period.

[2] Return frequency – type indicators have been published by i.a. European Central Bank and the central banks of Albania, Bulgaria, Norway and Poland.